Jennifer Mims, Strategic Consulting – Asset Management, Jacobs

With the advent of asset management (AM) as a discipline some 40+ years ago, structured approaches have developed to assure stakeholders that AM activities derive value. In the aviation industry, an effective AM programme improves customer service by increasing on-time performance and travel experience predictability. With Covid-19 affecting the market, the aviation community needs the most efficient and economic use of their assets and infrastructure more than ever.

The business of providing public aviation services is costly and complex. The industry relies heavily on infrastructure such as aircraft pavements, terminal buildings, utility distribution systems, roads, ancillary facilities, vehicles, special systems and technologies to provide these essential services to passengers and cargo transporters. The most pressing challenge is to ensure cost-effective management of these assets and the prioritisation of programmes due to reduced capital and operating budgets. Other challenges include the management of asset-related risk while infrastructure is aging, and public scrutiny is focused on environmental and social concerns.

Pressure on the aviation industry due to the pandemic intensifies these issues, and effective maintenance programs and focused capital projects will likely replace new development and expansion in the near-term. Organisations that employ asset management principles, including having thoughtful asset strategies and plans in place, will likely outperform during this transition and move forward more effectively once the industry recovers.

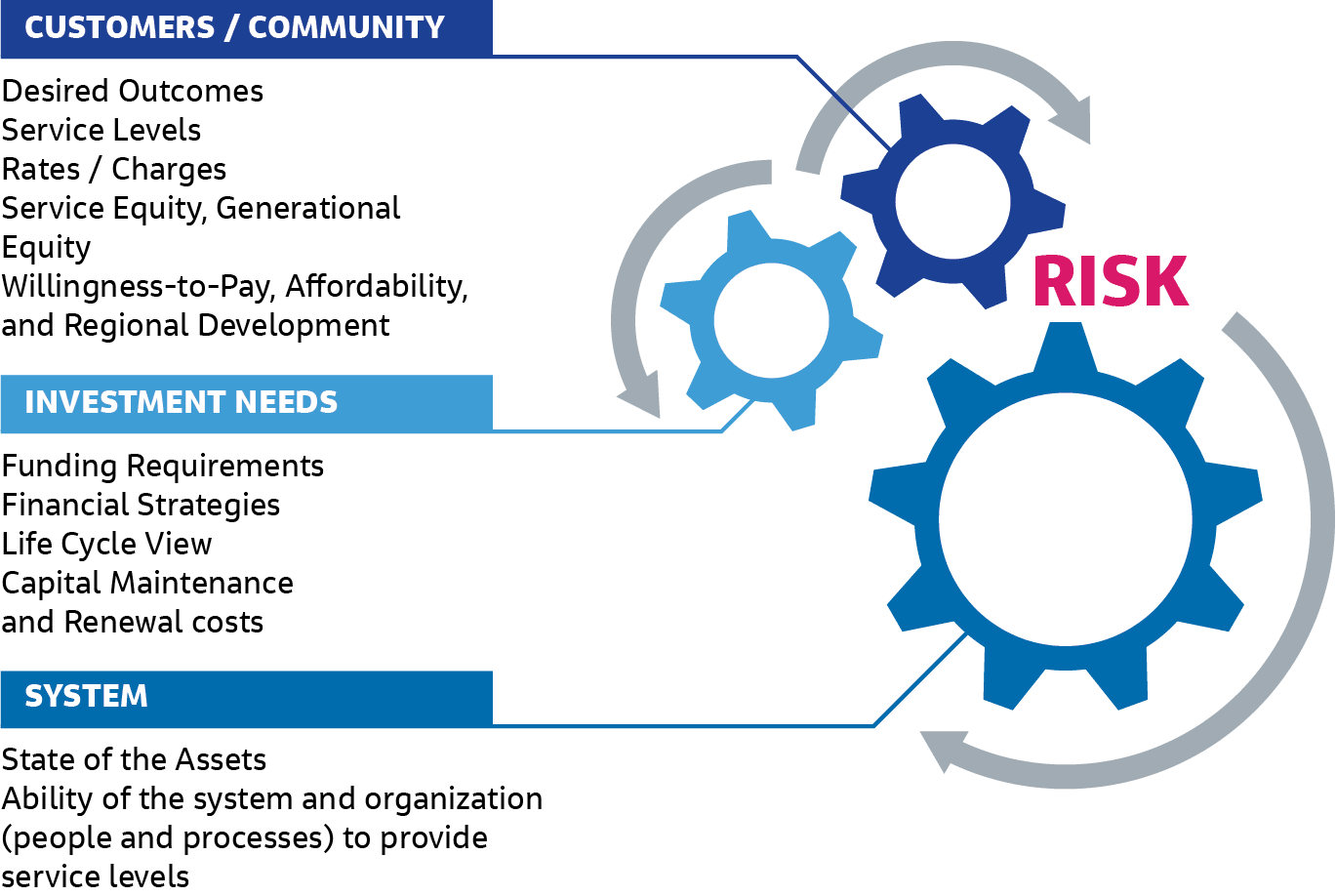

Although organisations have different reasons for improving the way they manage assets, the broad goal of AM is to understand:

Every organisation deciding to implement or maintain an asset management program works within unique demands, requirements, priorities, and constraints. Aviation AM is influenced by a number of factors that form a distinct operating, planning, and maintenance environment. From the wide range of asset categories to overlapping regulatory requirements (local, federal, industry), Jacobs has a vast amount of experience with factors like these and their relationship to AM principles. Read more >

Many benefits of improved AM are readily quantifiable. There are also benefits that are of equal value but less straightforward to quantify in monetary terms such as risk reduction, improved safety, system resiliency, standardisation, better ability to communicate budget needs, enhanced communication with stakeholders, knowledge management, employee satisfaction, and public trust. Assurance in planning and engineering processes and clear ownership and accountability enabling better recovery in a disruption event, are further benefits.

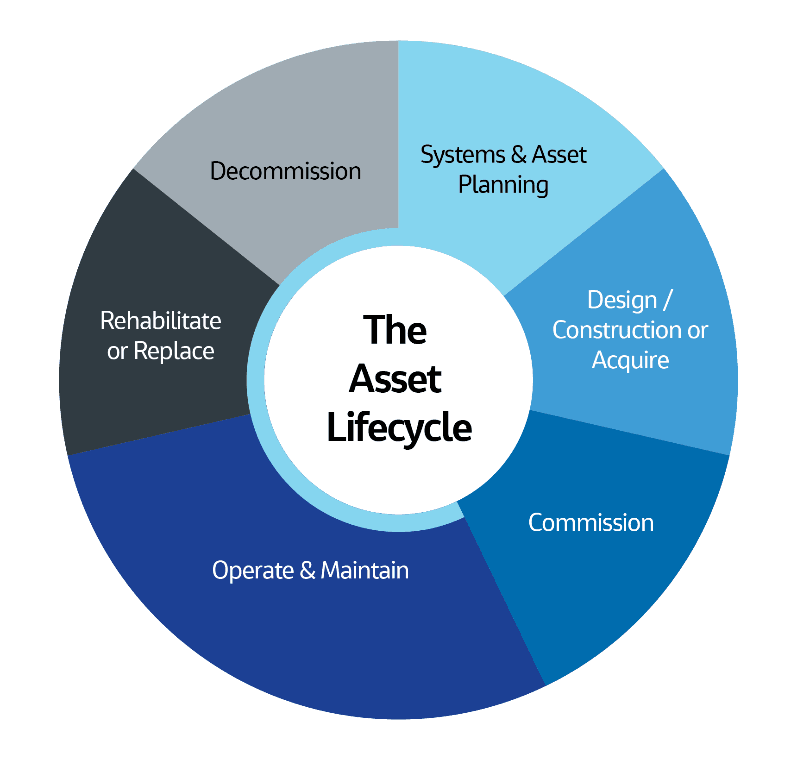

Jacobs’ proven approach to strategic AM results in cost saving and increased productivity by reducing ownership costs across the entire asset lifecycle and optimising the use of available budgets. We have led efforts at many airports across the globe to increase asset reliability and facilitate safety improvements through the use of data-driven management to predict and prevent failures as opposed to find and fix. We helped a major airport on the U.S. west coast significantly increase their predictive and preventive work on assets resulting in reducing overtime cost and at another U.S. airport, we helped lead the ISO 55001 certification process, reducing risk and consequence of failure for critical airport systems. At yet another, we collaborated with the terminal modernisation programme design team to incorporate changes that will have long term impact on cost, safety and reliability.

When effectively converted into information, data is key for organizations intending to operate based on AM principles. The value of the data is based on the level of influence it has – or has potential to have in the future – over investment plans. Improving the accuracy, completeness, and accessibility of asset data increases the confidence level in the resulting decisions. The procurement of AM tools, coupled with the optimization of data capture, business processes, and information analysis, can reduce risk and lifecycle costs. As an organization’s asset management practices mature, the technology tools required to support asset management become more complex to leverage the value of the data and provide incremental benefits.

For asset management principles and practices to be successfully and sustainably ingrained into an organisation’s business processes, the decision-making habits of staff and management during day-to-day work, the purpose of asset management and its benefits must be understood and embraced. AM activities must be consistent and coordinated across functional areas and across asset lifecycle stages. Staff and management must also have the knowledge, skills and willingness to adopt new methods of executing their work. Enablers – broad categories of functions and the key resources that will enable the organisation to institutionalise AM – include performance management, asset management governance, asset management competencies and training, organizational change management, and communications.

A strong asset management framework based on industry best practices makes business sense for any aviation organisation. While each organisation must determine how to define value and choose how to manage its assets to derive the best investment return, an approach based on best practice asset management principles will help achieve desired outcomes.

How can Jacobs help you? Contact Jennifer Mims at Jennifer.Mims@Jacobs.com and Andrew Gibson at Andrew.Gibson2@Jacobs.com