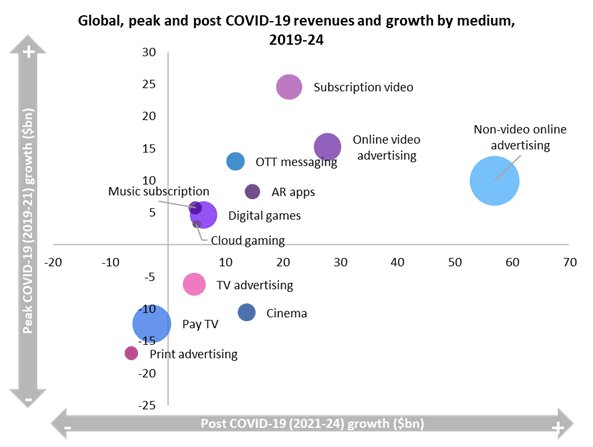

As the world hopes that 2021 will be defined by a successful rollout of a COVID-19 vaccine, one outcome is certain: growth of digital entertainment and consumer tech will accelerate. While revenue from TV advertising and cinema start rebounding, their growth will be far outpaced by that of online advertising and subscription video and rivalled by that of more nascent media such as augmented reality (AR) and over-the-top (OTT) messaging apps. Revenue from online advertising will rise by 9% to $368 billion in 2021. Video, music, and cloud-gaming subscriptions will generate $97 billion, up 16%, with revenue from cloud-gaming nearly tripling. Online video will play a critical role, directly driving $151 billion in subscription and advertising revenue, and acting as a key element or enabler of OTT messaging, AR and cloud-gaming services. All consumer tech players must consider how their services could be transformed—or disrupted—by these powerful forces.

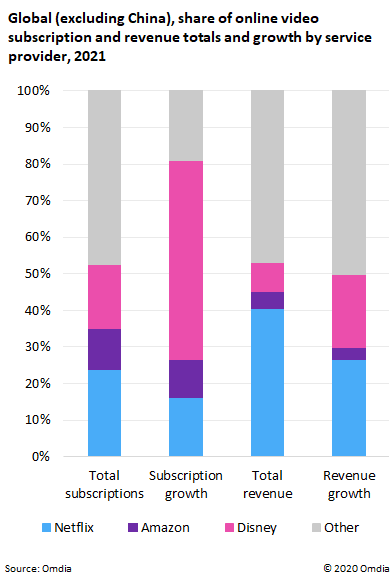

The window of opportunity in the online subscription video market will narrow in 2021 due to the phenomenal success of just three companies: Netflix, Amazon, and Disney. While consumers worldwide can select freely from a growing pool of global and local online subscription video apps, most tend to pick a combination of Netflix, Amazon, and Disney+. In 2021, each will be widely available as Amazon and Disney roll out services to new markets. By year-end, the three companies will account for over half of paid online video subscriptions and revenues worldwide, excluding China where the US companies’ apps are not available. In mature markets, their combined market share will be 65-70%. Netflix will remain the largest, with 216 million paid subscriptions, followed by Disney with 159 million and Amazon with 103 million. The three will also secure the majority of growth, accounting for about four out of five net new subscriptions (81%) and one out of every two net new dollars spent (53%). Disney alone will account for over half (51%) of net new subscriptions.

Any challengers must plan to co-exist with Netflix, Amazon, and Disney. This should involve focusing on content and experiences that the three don’t currently provide, but also accepting that much of many subscribers’ time and money will already be spoken for.

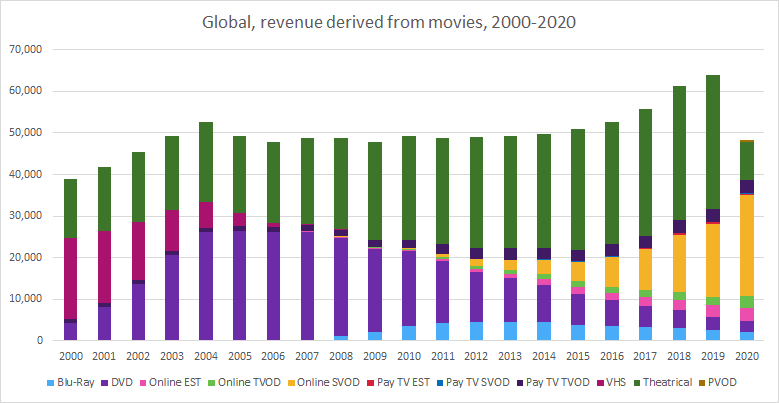

The crisis facing movies is essential rather than existential. Despite COVID-19’s devasting blow to cinema-going and production in 2020, movies will remain a critical feature of the cultural landscape and entertainment business in 2021 and beyond. The critical question the industry must answer is: what are movies for? Cinema will endure, simply because so many want it to, from film-makers to producers to studios to governments and, of course, consumers. Box office revenues will reach $19 billion in 2021, up 106% on 2021, as lockdowns ease and pent-up demand leads growing numbers to return to theatres, especially to see blockbusters originally due for release this year. But box office revenues will not return to pre COVID-19 levels until 2024, falling short by $13 billion in 2021 compared to 2019. Growth from subscription video on-demand (SVOD) and premium video on-demand (PVOD) services that allow consumers access to titles usually reserved for cinemas will go some way to closing the gap in 2021, but far from all. In 2021, studios must think carefully about what they want to achieve with movies. This will partly be about how to harness SVOD and PVOD without undermining theatrical, but also how to evolve, expand, and combine cinema and home entertainment experiences.

The games industry has a problem, albeit a good one. Almost every facet of the market—console, mobile, subscriptions, cloud, AR, VR, and esports—will perform strongly in 2021, making the classic strategic question “where to play” hard to answer. Console hardware and software revenue will rise by 5.2% to $36.3 billion thanks to the recent launch of Sony’s PlayStation 5 and Microsoft’s Xbox Series X. Cloud gaming will also have a breakthrough year with vital pieces finally coming together, with spend reaching $4 billion, a 188% increase on 2020. Crucially, cloud-gaming services will add to the on-console gaming experience while attracting a slew of casual gamers who do not own consoles or PCs. AR, VR, esports, live-streaming, and so-called metaverses like Epic Games’ Fortnite, meanwhile, will enable gaming to further permeate the consumer world, with consumers choosing to spend more of their time and money immersing themselves in video game worlds and culture than on other media.

The dilemma games companies must face is how best to monetize their content while juggling the often competing aims of finding the widest possible audience, maintaining goodwill from that audience, and not sacrificing too much control to other platforms.

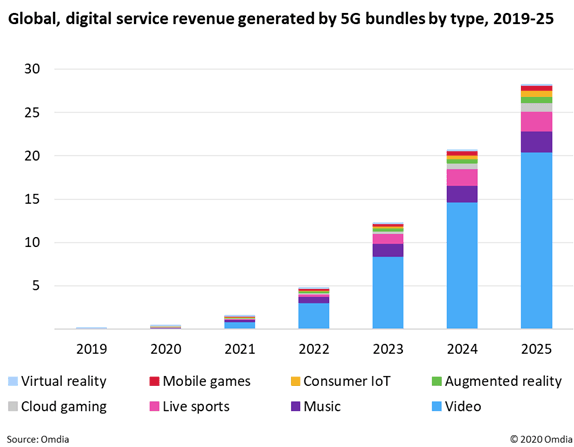

Super-aggregation is not new to entertainment. It arguably dates back to the arrival of the pay-TV bundle over 30 years ago and has more recently found forms in Amazon Channels and telco bundles of Netflix and mobile services. In 2021, an array of industry players will broaden the concept’s horizons and intensify its competitive impact. Activity will broadly fall into three camps. One, network operators extending their bundles of third-party apps and pay TV, home broadband and mobile beyond video and music to cloud-gaming and other emerging digital services. Two, tech firms aggressively marketing own-brand “mega-bundles”, such as Amazon Prime and Apple One. Three, the same tech firms building out existing and new ways to aggregate third-party apps, such as Amazon Channels and Apple TV, with Google likely to make increasing moves towards the model. Much of this activity will overlap. Operators will bundle the likes of Amazon Prime and Apple One and tech giants will encourage pureplay app providers to embrace their platforms. 5G bundles will play a key role, delivering a modest $1.5 billion of digital service revenue in 2021 (see figure) while laying foundations for partnerships that will deliver over $67 billion over the next five years as uptake of the mobile technology accelerates.