A “Gentler Form of Capitalism” and Its Failure to Prioritize, by Martin Grosskopf of AGF Investments

One of the key challenges for Environmental, Social and Governance (ESG) investing, at least in its still-early stage, is that it has always been a movement in search of a philosophy. True, it has a goal: since the “mainstreaming” of ESG began in the early 2000s, it has sought to bring important social and environmental issues into the “market mentality” around risk and return. Lately, the movement has claimed some significant victories, including the push for climate change disclosures (such as those recommended by the Task Force on Climate-related Financial Disclosures), the recent movement towards stakeholder capitalism, and the newfound market appetite for funding all things ESG-related.(i)

The general tone of ESG throughout its history has been to encourage a gentler form of capitalism, but its underlying philosophy has been completely in line with the main tenants of the prevalent market philosophy – that markets are the most efficient way to allocate capital, at least over time, and that they will do so in an ultimately rational fashion that will eventually see the goals of ESG realized. Perhaps part of this conformism is simply practical; after all, underfunded pensions have little fiduciary room to do much more than tinker with the system.

The current crisis, however, presents an opportunity for a much deeper assessment of the role of markets, governments and, for that matter, ESG. Following only 12 years on from the last big public-sector intervention – the Great Financial Crisis (GFC) – events occurring in only a few short weeks have laid bare the limits of efficient-market theory and the market’s inability to perform its most basic function: deploying capital to its highest and best use. That is not only evident in the disconnect between equity market over-performance and dismal economic realities; it also lies in the failure of markets to prioritize issues such as healthcare capacity and environmental health over austerity. And this failure comes despite the mainstream emergence of ESG and its successes.

Clearly, some self-reflection is needed to recognize the limited capacities of ESG to effect meaningful change within the market dynamic, and also to address the balance between returns and social/environmental impact. Orthodoxies that evolved to reward shareholders (ESG-inclined or otherwise), including low tax rates, ever-increasing dividend payouts, low reinvestment and share buybacks, will need to be modified to reflect the reality of a government backstop and the social contract implicit in worker obligations.

If it functions only as an add-on to the prevalent market philosophy, ESG cannot inform on the balance between shareholder rewards and societal resilience. The COVID-19 pandemic, as the first truly global natural disaster of the modern era, has demonstrated that the current skew towards shareholders is exceedingly fragile, and changes are likely required that go far beyond the World Business Council’s acknowledgement of a stakeholder model.

In response to the COVID-19 crisis, governments have proven that when sufficiently motivated, they are willing to deploy apparently unlimited resources to address issues of social risk. Ideas that were viewed as fringe only months ago are not only accepted now, but rolled out on a scale that was once-unimaginable even by their proponents. Modern Monetary Theory, for example, challenged the conventional logic around government deficits and austerity. Over the past ten months, the International Monetary Fund notes that governments have deployed close to US$12 trillion in various measures not to defeat the virus – of which clearly there could be variants or recurrences – but to buy time for an underfunded health system to respond effectively. In the most dramatic instance, governments are directing funds to largely replace income for at least some workers, in effect providing a basic income provision.

If governments can demonstrably print and deploy money at will, then it suggests that “austerity” was something of a poor excuse for the significant social spending cuts we have seen over many years.

It also now seems untenable to argue that the extraordinary efforts governments have made to prevent COVID-related deaths should not also be taken to address other pressing social-environmental threats, such as hunger, air pollution, poor sanitation, and so on. For longer-tail issues such as climate change, it becomes less believable to claim that mitigation efforts cannot be funded or that the most impacted industries cannot be transitioned. In response to a natural disaster, and in a short period of time, society has shown the desire and means to radic ally alter patterns of work and leisure. Science has in effect taken prominence in informing societal actions, perhaps foreshadowing a wider recognition of its vital role in dealing with climate change as a large-scale systemic risk.

What are the implications for ESG? A pain point for “ESG 1.0” is its current philosophical interlinkage with traditional market orthodoxy. Post GFC, there was ample evidence of “models behaving badly,” yet these models continued to inform asset allocation and investment decision-making in the following years.(ii) Consistent with its history, ESG has largely been applied as a modest adjustment to these models instead of a methodological alternative. For this reason, it has not really prevented or reduced systemic risk – as COVID-19 has made amply clear. Generally, ESG has been added to the lexicon of efficiency – supporting global supply chains, conventional asset allocation and low tracking error, and perhaps adding some alpha – but has not enhanced the systemic resilience in the meaning of scholar Nassim Taleb and increasingly hoped for in initiatives such as the Financial Stability Council.(iii)

That the early link between ESG and market philosophy was important is undeniable – if only because it legitimized mass adoption of ESG practices. However, if we learn anything from the last two crises, it should be that we are not likely to predict the next one, whether ESG is adopted more broadly or not, so this should not be the primary aim of “ESG 2.0” if we hope that it will contribute to societal and environmental resiliency. If they hold that hope in earnest, ESG practitioners will need to forcefully engage on the relative roles of shareholder, government and workers not just with each other, but also with the asset allocators and real decision-makers within their organizations. This will involve very tough discussions around margin-friendly “efficiencies,” the realism of return expectations and growth rates, and recognition of the heavy capital intensity of an energy transition.

If these discussions do evolve, some of the current tenets of ESG practice will change:

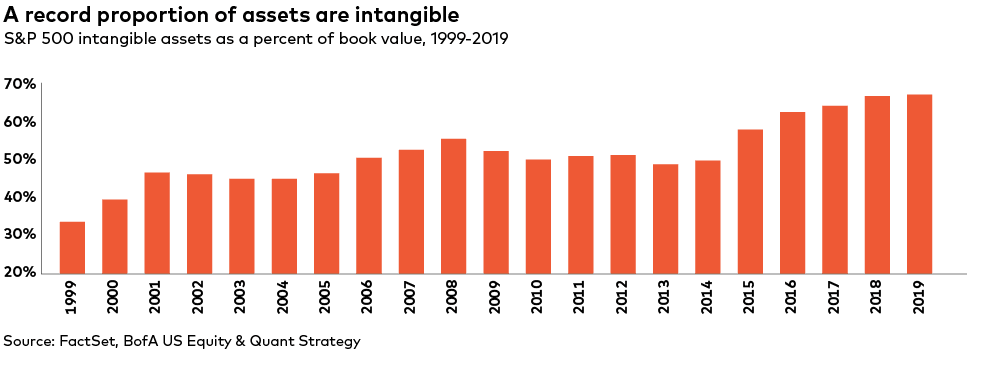

Broad recognition of ESG as a useful and early “alternative” data set – The origins of ESG data collection in the 1990s lied in the recognition by some, generally outside the mainstream, that conventional financial data did not measure the full cost or benefit of a company’s interaction with society and the environment. In fact, MSCI ESG research is based on the Intangible Value Assessment (IVA) developed by Innovest in the 1990s, which along with Jantzi Research (Sustainalytics) was an early harbinger of the increased measurement of intangibles generally within the market over the following 20 years (Figure 1). Broader usage of the data will ensure improved data and reporting, but will also enable broad recognition of the value of incorporating at least a portion of this alternative dataset into relative valuation and asset allocation decisions.

The linkage between ‘asset-lite’ business models and high ESG ratings will become obvious – A source of alpha for many ESG-oriented funds has been derived from the strong link between ‘asset-lite’ business models and high ESG ratings. Clearly firms that employ fewer people per dollar of revenue (lower human capital intensity) and who provide software or cloud services tend to have a lower direct operational footprint relative to those in manufacturing or retailing industries. The alpha associated with this linkage is likely to become obvious to market participants, making it less likely to be a source of alpha in the future.

The efficacy of “relative” scores will decline – So far, the relative performance of firms on ESG metrics has been meaningfully different. During the latest decline, companies with better ESG scores have outperformed. This reflects the reality that within any given sector, some companies are taking ESG risks and opportunities seriously and devising explicit strategies to improve or capitalize. Over time, however, the tendency in any industry is towards convergence on issues that are viewed as material.

For example, if board diversity really is a strategic advantage, all companies will tend to adopt diversity practices. So, imagine a future in which all boards are diverse – and then imagine trying to distinguish materiality among diversity strategies. Or consider climate change. The years of fighting a rearguard action for resources companies will likely morph into credible – and widely adopted – strategies for reducing their carbon footprint and assisting with the energy “transition” (lower emitting sources). Whether used for long-only strategies or those employing shorting, over time the efficacy of a simplistic interpretation of ESG data points is less and less likely to be meaningful.

ESG progress will be defined as co-operation, not competition –

As the COVID-19 pandemic has demonstrated, systemic risks such as natural disasters cannot be addressed competitively at the company level. Inter-company rivalry does not help improve health outcomes or reduce the burden of employee furloughs on societal balance sheets. Universal owners (meaning large pension funds) do not want human capital to be a competitive factor, but they do want standards to rise across society. Similarly, oil companies must cooperate with one another and with governments to meaningfully introduce alternatives and reduce dependence. This co-operative activity will overwhelm the relative ESG analysis of company operations, since the differences in operational emissions pale in comparison to credit risks associated with systemic demand declines.

Sustainability themes will continue to provide a strong lens –

In today’s crisis, government is prioritizing industries that it deems essential. Ironically, this trend is entirely congruent with the rise of “impact” investing. As today’s focus on data quality, disclosure and corporate structure standardizes by market cap and sector, emphasis will shift to the purpose of the company itself. After all, manufacturing ventilators or discovering vaccines is not the same as making products that increase respiratory risk, such as tobacco or combustion pollution; from an impact perspective, that the cost of capital for one should be lower than the other is aligned with societal objectives towards resiliency and health and well-being. Applying a thematic lens can capture these long-term trends while steering through shorter-term cycles and can provide a more predictable basis for outperformance.

Just as every bear market and recession provides the inevitability of recovery, the current crisis may be an appropriate end to ESG 1.0 and a beginning for ESG 2.0. We are hopeful that ESG 2.0 can build on the successes of the last 20 years, while contributing meaningfully to a market philosophy that rewards shareholders but equally emphasizes the importance on government and workers. Our common future may depend on it.

Martin Grosskopf is a Vice-President and Portfolio Manager at AGF Investments Inc, he manages AGF’s sustainable investing strategies and provides input on sustainability and environmental, social and governance (ESG) issues across the AGF investment teams. He is a thought leader and a frequent public speaker on ESG and Green Finance issues. Martin has more than 20 years of experience in financial and environmental analysis. He manages the AGF Global Sustainable Growth Fund which is available through the AGF Global Sustainable Growth ETF (AGSG). He is a regular contributor to AGF Perspectives.

References:

i https://www.wbcsd.org/Overview/News-Insights/Insights-from-the-President/The-triangle-that-will-fix-capitalism

ii https://www.amazon.ca/Models-Behaving-Badly-Confusing-Illusion-Reality-Disaster/dp/1439164991

iii https://www.fsb.org/

The commentaries contained herein are provided as a general source of information based on information available as of June 18, 2020 and should not be considered as investment advice or an offer or solicitations to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Investors are expected to obtain professional investment advice.

The views expressed in this blog are those of the author and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds or investment strategies. AGF Investments is a group of wholly owned subsidiaries of AGF and includes AGF Investments Inc., AGF Investments America Inc., AGF Investments LLC, AGF Asset Management (Asia) Limited and AGF International Advisors Company Limited. The term AGF Investments m ay refer to one or more of the direct or indirect subsidiaries of AGF or to all of them jointly. This term is used for convenience and does not precisely describe any of the separate companies, each of which manages its own affairs. ™ The ‘AGF’ logo is a trademark of AGF Management Limited and used under licence.