By Praveen Jagwani, CFA CEO, UTI International Pte Ltd.

‘Buy Low- Sell High’ is the fundamental formula for success in any trade and the stock market is no exception. Investors are forever in the hunt for markets that are going cheap because a bargain has universal appeal.

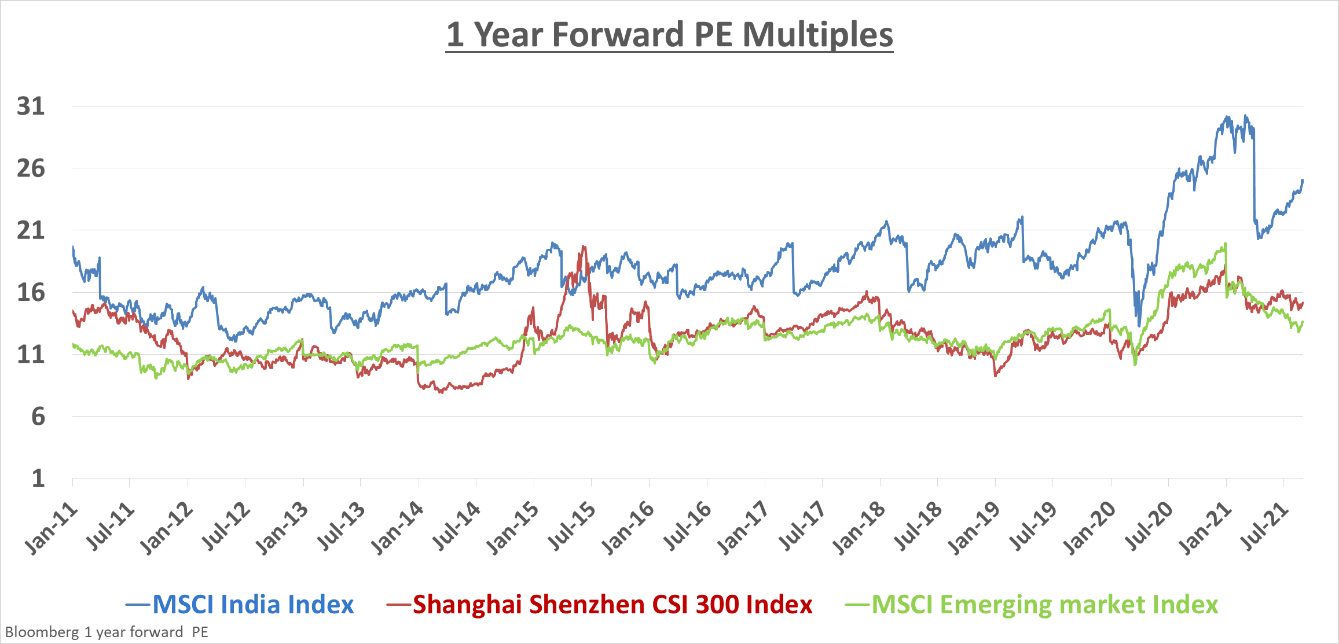

On that metric, India has never attracted bargain hunters, for India’s PE multiple has always been expensive. As Chart-1 shows, in the past 10 years, India has consistently traded at a higher PE ratio (1 year forward Price-Earning multiple) than the Chinese market or indeed the entire Emerging market set of countries.

On average, over the past decade, India has traded at a 36% premium to the EM index. As a consequence, the majority of the global investors, in single-minded pursuit of the "cheap" have shunned India. Had these investors been right, their decision to avoid India should have been handsomely rewarded.

Chart One

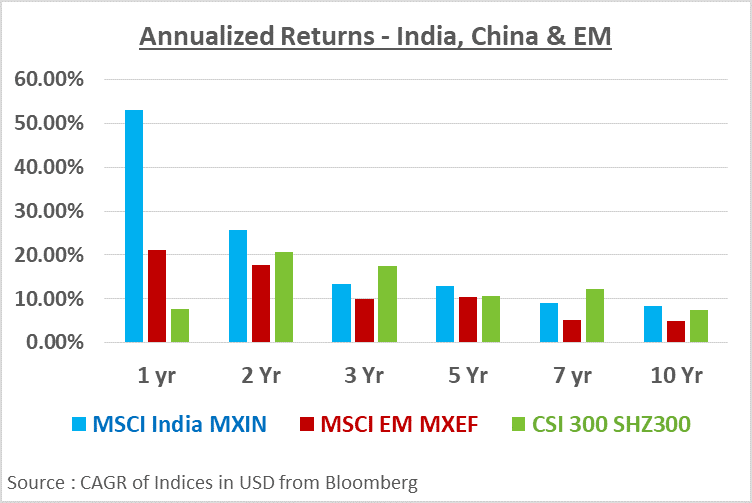

However, as Chart-2 shows, India has consistently delivered higher annualized returns than the Emerging Markets Index across all time periods. India has also performed better than China, for the most part. Cumulatively over the past 10 years, in US Dollar terms, MSCI India has returned 124% as against 66% by MSCI EM and 106% by CSI300 of China.

Chart Two

Evidently, those who have pursued a PE-multiple based screening criterion have been consistently wrong about India. That begs the question: What can we expect in the next 3-5 years, given that Indian equity valuations continue to be perched at all-time highs?

India’s valuation is undeniably rich and yet we believe that India is likely to deliver higher equity returns than its EM Peers. For the past 10 years, corporate earnings have grown by an anaemic 5% p.a. but India has now entered a new cycle of super-growth. I expect corporate earnings and therefore equity returns to be in the mid-teens for the remainder of this decade. There are four key reasons for this conviction:

Beijing, on the other hand, is not prioritising growth as it once did. It is instead trying to rein in unbridled capitalism and reduce the economy’s dependence on debt. The crack-down on its tech companies and industry chieftains is emblematic of the third-world regulatory uncertainty detested by global investors. While the ‘Common Prosperity’ agenda is laudable, it will mean that China is unlikely to be the engine of global growth it was after the 2008 financial crisis.

So who is going to power the next round of global recovery? At the moment, all signs point to India. India has the scale, stability, institutionalized frameworks of governance and is a liberal democracy to boot. It has demonstrated that it has the aspiration and the resolve to counter-balance China in the Indo-Pacific. As a result, both foreign direct investments as well as portfolio investments have been pouring into India at an unprecedented rate. In 2020, India attracted $64 billion in foreign direct investment, the fifth-largest inflows in the world, according to the World Investment Report 2021 by United Nations.

This trend is likely to accelerate as India commands an ever-increasing piece of the Emerging Market GDP as well as Market Capitalization. But it won’t be a linear progression. Expect much volatility as the world wrestles with the withdrawal pangs from years of easy money. The indices will swing as global sentiment oscillates between Risk-On and Risk-Off but if you have a 3 to 5-year outlook, India will reward those who have a 3 to 5-year time horizon.

In summary, China seems to be abdicating its spot as the world’s reliable growth engine. India is being thrust to assume the mantle as it enters a rising earnings cycle, predicated on various domestic and global drivers. Such a cycle is characterized by enhanced shareholder returns. Investors would be well-advised to increase their exposure to Indian equities even though they don’t appear cheap.