Amy Kessler, Senior Vice President and Head of Longevity Risk Transfer Rohit Mathur, Vice President and Head of International Transactions Prudential Financial, Inc. (PFI)

It’s not often that crises come about, but when they do, companies who are prepared and ready to respond will stand out from the crowd. In this article, Amy Kessler, Senior Vice President and Head of Longevity Risk Transfer, Prudential Financial, Inc. (PFI), and Rohit Mathur, Vice President and Head of International Transactions, PFI, examine long-term de-risking plans, assess the success of these strategies, and how they aided companies in their preparations for crisis situations like pandemics.

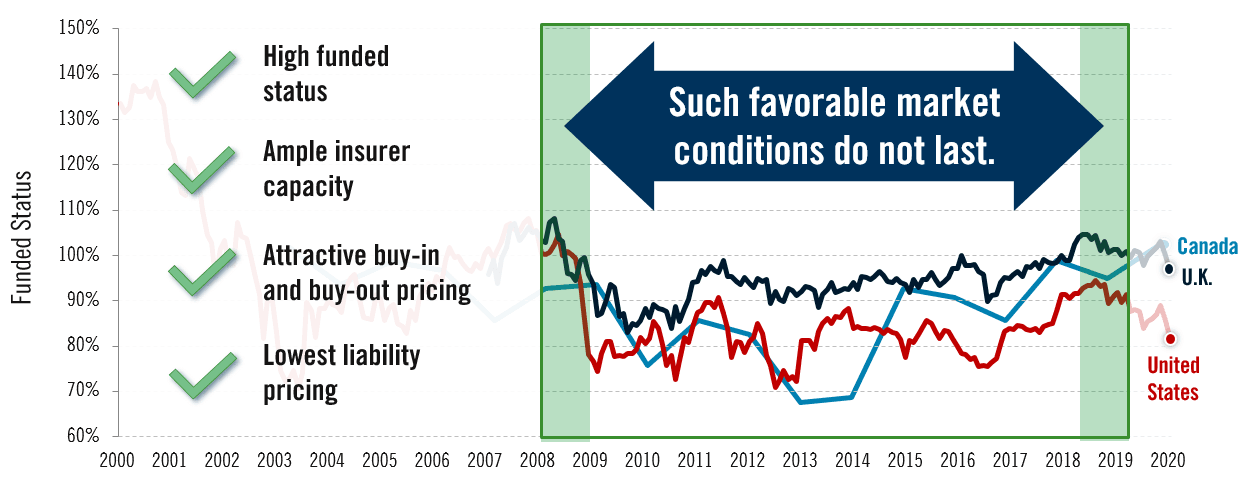

We are in the midst of incredible uncertainty. The coronavirus has shaken global markets and communities, impacting the daily lives of citizens, the economic stability of small businesses and corporations, and the funded status of many pension funds. In 2019, U.S., U.K., and Canadian pension funds were simultaneously at the best funded status they had experienced in ten years as shown in Figure 1, but in 2020 funded status in the U.K. and U.S. has fallen dramatically with a massive increase in market volatility.

U.S. Source: Milliman 100 Pension Funding Index; the 100 largest U.S. corporate pension plans, February 29, 2020 (82.2%) Canadian Source: Aon’s Median Solvency Ratio, Canadian DB Plans as of December 31, 2019 (102.5%). FTSE 100 Source: Aon Hewitt, “Aon Hewitt Global Pension Risk Tracker,” as of February 29, 2020 (96.9%). https://PensionRiskTracker.aon.com, accessed March 12, 2020. Funding ratio (cumulative assets/liabilities) of all pension schemes in the FTSE 100 index on the accounting basis.

In uncertain times, pension de-risking is an all-weather solution for our corporate client base. Well-funded pension plans with high allocations to fixed income are experiencing much greater stability in their funded status. In fact, in the wake of recent turbulence, one client communicated to us that the prior de-risking of their plan was one of the most important strategic decisions the company has ever undertaken.

We’ve worked with many companies toward their de-risking goals over a decade or more, punctuated by major market disruptions. While volatile markets like the one we’re experiencing today may pull companies farther away from achieving their de-risking goals, we know that sponsors remain committed to de-risking their plans. In fact, volatile markets like these often bring opportunity, so it pays to be prepared. While there can be various incentives to reduce or transfer risk, we believe low interest rates, widening credit spreads, weakening currencies, and mortality volatility all present unique opportunities.

With low rates, many highly rated sponsors can issue corporate debt at attractive yields and deposit the proceeds into the pension fund to improve funded status. Since the pension deficit is already considered debt of the corporation, this debt-for-debt exchange is likely to be considered credit neutral by rating agencies and stakeholders, though it can be credit positive if it allows the sponsor to take meaningful steps to de-risk the plan. For U.S. plans, it also eliminates variable Pension Benefit Guaranty Corporation (PBGC) premiums, which equal 4.5% on pension deficits. While these “borrow to fund” strategies may not work for most in the current environment due to widening credit spreads offsetting the benefit of low rates, this can be an important strategy in a post-pandemic environment. Companies can monitor markets and be ready to transact once spreads tighten.

Another opportunity arises when falling risk-free rates are combined with widening credit spreads. These market conditions often mean the economy is in distress, but for pension funds holding a cash flow- or key-rate duration-matched portfolio of high-quality bonds, the interest rate risk is largely hedged. Gilts, treasuries, and other high-grade bonds will likely appreciate if rates fall, and if, at the same time, the economy is in trouble and credit spreads widen, there is a real opportunity to transfer risk as pension buy-ins are backed by spread-bearing assets. Buy-in pricing is favourable when it has an implied return above gilts or treasuries, and when credit spreads widen, buy-in pricing generally improves. It is an excellent relative value trade for a pension fund to use freshly appreciated government bonds to pay for a buy-in that returns risk-free plus a wide spread. This trade locks in the spread to government bonds implied in the buy-in price. This locked-in gain increases funded status after the buy-in is complete and transfers all risk to the insurer.

It can be very cost-effective for a multinational plan sponsor to plug a pension deficit in a country with a weakening currency. Using the U.K. as an example, a multinational company headquartered outside of the U.K. that has a U.K. pension plan can more easily close a funding gap in the plan after the pound (£) depreciates. Since the first Brexit vote, the cost for a U.S. parent to plug a deficit in a U.K. plan has gone down by roughly 25%*. The same logic holds for funding risk transfer premiums. Today, a U.S. parent with a U.K. plan can fund a buy-in premium for roughly 25% less than in early 2016. Many companies will be focused on conserving cash during these uncertain times. However, post pandemic, should we encounter a U-shaped or V-shaped recovery, this could be a key de-risking opportunity.

*Source: Prudential Financial, Inc. (PFI) analysis of currency change from Brexit vote through March 23, 2020.

We have seen very low longevity improvement in recent years. Over a seven-year period from 2011 through 2018, there was only a modest 2.5% improvement in the U.K. As a result, insurer and reinsurer pricing has decreased and many U.K. pension schemes are bringing longevity swaps to market. One pension fund that took advantage of this opportunity was the HSBC Bank U.K. Pension Scheme. In 2019, HSBC completed the third largest longevity risk transfer transaction ever in the market at £7 billion ($8.7 billion) with The Prudential Insurance Company of America (PICA). The arrangement is scalable and repeatable.

While many plan sponsors are navigating today’s turbulent market environment, they can take courage in The Rolls-Royce U.K. Pension Fund’s ten-year journey to de-risk. Back in 2011, after recovering from the financial crisis and de-risking its assets, Rolls-Royce entered into a £3 billion longevity swap for retirees in its pension scheme. The 2011 swap was arranged by Deutsche Bank and reinsured by PICA and several other reinsurers.

Fast forward to June of 2019, and after more than a decade of steady steps toward a lower-risk future, Rolls-Royce was nearly ready to complete a buy-out. It took nearly a year of monitoring the market, but it pays to be prepared and Rolls-Royce completed a £4.6 billion buy-out with Legal & General (L&G) that included the retirees covered by the 2011 swap. To make the buy-out work, the pre-existing longevity swaps from 2011 had to be transferred from Deutsche Bank to L&G. The transfer of the earlier contracts is known as “novation.” In order to capitalise on near-perfect market conditions, both the buy-out and the novation of the existing contracts were completed within weeks of the decision to transact, proving that longevity swaps can be used as a stepping stone to a full risk-transfer strategy. Rolls-Royce faced setbacks along the way, but by remaining committed to de-risking, it ultimately transferred its pension obligations before the market fell away.

Markets in which all factors are positive are anomalies, and the favorable market conditions we saw in 2019 have proven to be fleeting. For many defined benefit pension funds, the 2020 crisis will represent a setback on the road to a lower-risk future, but it is important to stay the course: to continue prudent risk management actions with appropriate investment portfolios, and to set a realistic price target for pension risk transfer, while monitoring funded status and insurer pricing as markets stabilise. Pension funds with the potential to transact should then be prepared to pull the trigger to transact on short notice when their price target is met.

For more information on the opportunities and case studies in this article, please contact Rohit Mathur at rohit.mathur@prudential.com.

This article has been prepared for discussion purposes only and does not constitute an offer or an agreement, or a solicitation of an offer or an agreement, to enter into any transaction (including for the provision of any services). Prudential Financial, Inc. (PFI) does not provide legal, regulatory, tax or accounting advice. An institution and its advisors should seek legal, regulatory, investment, tax and/or accounting advice regarding the legal, regulatory, investment, tax and/or accounting implications of any of the strategies described herein. This information is provided with the understanding that the recipient will discuss the subject matter with its own legal counsel, auditor and other advisors. Insurance and reinsurance products are issued by either Prudential Retirement Insurance and Annuity Company (PRIAC), of Hartford, Connecticut, or The Prudential Insurance Company of America (PICA), of Newark, New Jersey. Both are wholly owned subsidiaries of PFI, and each company is solely responsible for its financial condition and contractual obligations. Neither PFI nor PRIAC nor PICA is affiliated with Prudential plc of the United Kingdom. Neither PRIAC nor PICA is licensed or regulated within the European Economic Area as a reinsurer. PRIAC and PICA do provide offshore reinsurance to companies that have acquired U.K. pension risks through transactions with U.K. plan sponsors. © 2020 Prudential Financial, Inc. and its related entities. Prudential, the Prudential logo and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide. Prudential Retirement is a PFI business. 1033236-00001-00