Robert Duncan, SVP Institutional Sales & Portfolio Manager, Forstrong.

If the first 4 months of the 2020s are any indication of what this new decade has in store for us, can we just skip to the 2030s now?

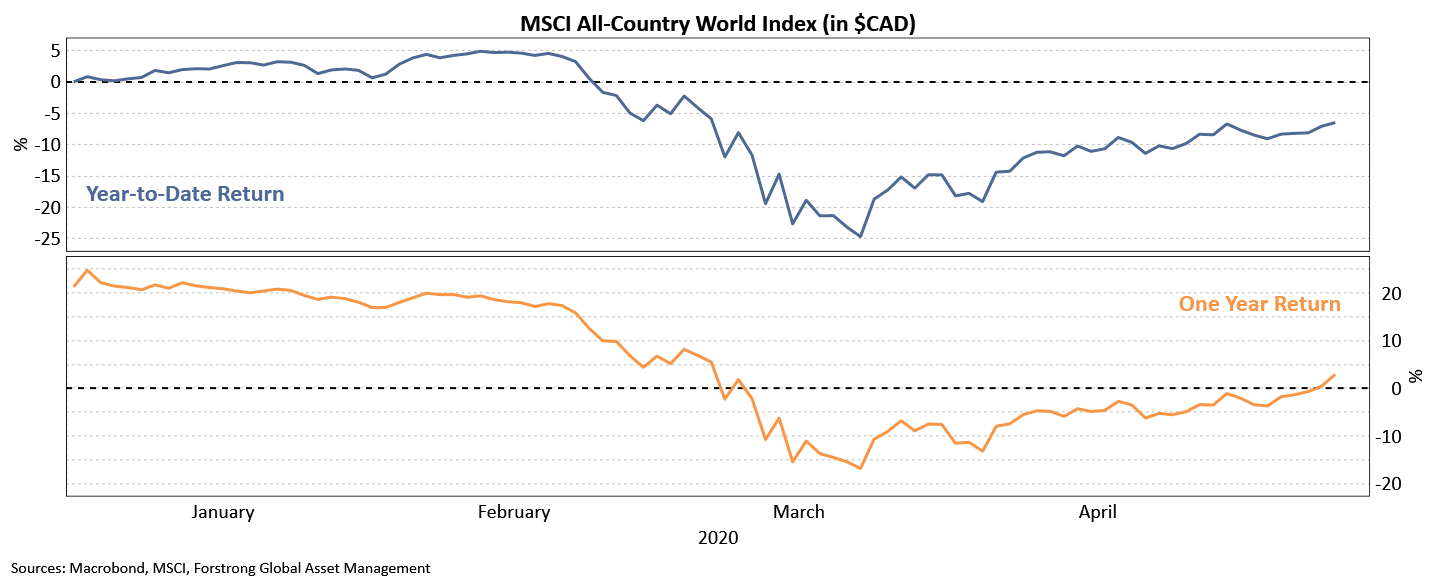

With everything that has already transpired, a spat of early-May snowstorms here in Toronto just added insult to injury. Personal grumblings aside, it may surprise some readers that despite the challenges we have faced this year, global stocks are within striking distance of their 2019 year-end levels.

Per the chart at the end of this article, the MSCI AllCountry World Index (in Canadian dollar terms) has lost 6.5% year-to-date, and remarkably has a positive one year return.

Many investors may find it difficult to reconcile this considering we are in the midst of a global economic shutdown.

Yet, as is typically the case, more nuanced action is happening beneath the surface in financial markets. New trends are underway – both negative and positive - that will stay with us beyond the pandemic.

Naturally, two questions come to mind: how did we get here and is the current situation sustainable?

In mid-March, our Investment Team convened for the regular quarterly strategy sessions. Methodically working through our investment process yielded what may seem like counter-intuitive results; namely increasing portfolio risk at a time when financial markets were melting down around us.

While it can be easy to panic during a crisis, our process once again kept client portfolios oriented to the right long-term perspectives and importantly, avoided a big mistake (the cardinal sin of investing is selling into a panic).

Our decision was supported by 3 key macro points: economic damage was likely to be severe but transitory, fiscal and monetary responses were unprecedented in terms of the size and speed of deployment, and finally, panic selling had disconnected financial assets from their intrinsic values. Additionally, notwithstanding investment professionals’ lack of formal epidemiology training, it was logical that widespread lockdown measures would be helpful in slowing virus transmission rates.

After a rapid and large rebound in almost all risk assets, the period ahead is likely to see more variation in specific asset class performances. And, pundits have pointed out that during many previous recessions and major market corrections, the bottom was re-tested at least once. A scenario where an overly hasty economic re-opening leads to another severe wave of viral outbreak could be a potential catalyst.

A flare-up in trade tensions between the US and China is another potential hazard as the Trump administration attempts to deflect blame for the handling of the pandemic response and capitalize on rising Sinophobic sentiment.

While cognizant of these risks, making investment decisions based on historical charting patterns and geopolitical risks alone is not a viable approach. Instead, we are also keeping a close eye on the corporate earnings outlook, default rates and unemployment claims to help gauge the health of the economy and its ability to bounce back.

We are confident that policymakers will continue to err on the side of accommodation, while depressed oil prices and interest rates will offer further relief to households and companies outside of the energy sector.

With such a wide range of potential outcomes on the horizon, maintaining a balanced asset mix approach is well warranted. We have increased exposure to cash and gold equities to enhance diversification and dampen portfolio volatility. Equity holdings have been tilted towards a higher quality positioning, with decreased exposure to small cap stocks as well as smaller, less liquid emerging and frontier market countries.