Greg Wasserman, Head of Private Climate Investing, Wellington Management

The root cause of climate change is the buildup in the atmosphere of greenhouse gases from human activities, such as energy generation, transportation, and industrial activity.

These gases trap heat and warm the planet, which leads to increased volatility and severity of heat, drought, storms, floods, and wildfires.

These weather events lead to societal disruption, such as displacement of people from their homes, power outages, supply-chain disruptions, and food insecurity.

The effects of climate change are accelerating. The past five years have been the hottest five on record. In 2020, we saw record wildfires in Australia and California, a record number of named Atlantic storms, and record water levels in parts of Europe and China. In May 2022, temperatures in New Delhi reached 49°C (120F).

According to the United Nations Intergovernmental Panel on Climate Change (IPCC), the world will reach an irreversible tipping point if the increase in global temperatures cannot be limited to 1.5°C, a level that would require “rapid and far-reaching” transitions in land, energy, industry, buildings, transport, and cities.

The latest projection from the World Meteorological Organization implies a 50% risk that the global temperature temporarily reaches that threshold in the next five years.

We believe addressing climate change requires a two-pronged approach. As society implements measures to mitigate the cause of climate change by reducing greenhouse gas (GHG) emissions, governments, businesses, and consumers need to adapt to become resilient to the extreme weather events we are already experiencing.

The challenge is clearly daunting. But that also means that the market opportunity for mitigation- and adaptation-related climate solutions is enormous and necessary.

While some individuals and companies may be willing to make trade-offs for more climate-friendly solutions, it is unlikely that society will accept trade-offs at the scale needed. People are unlikely to stop traveling and consuming, and businesses are unlikely to stop producing. Regulation will be essential, but, ultimately, we think solutions will need to be market-driven and stand on their own to be truly scalable.

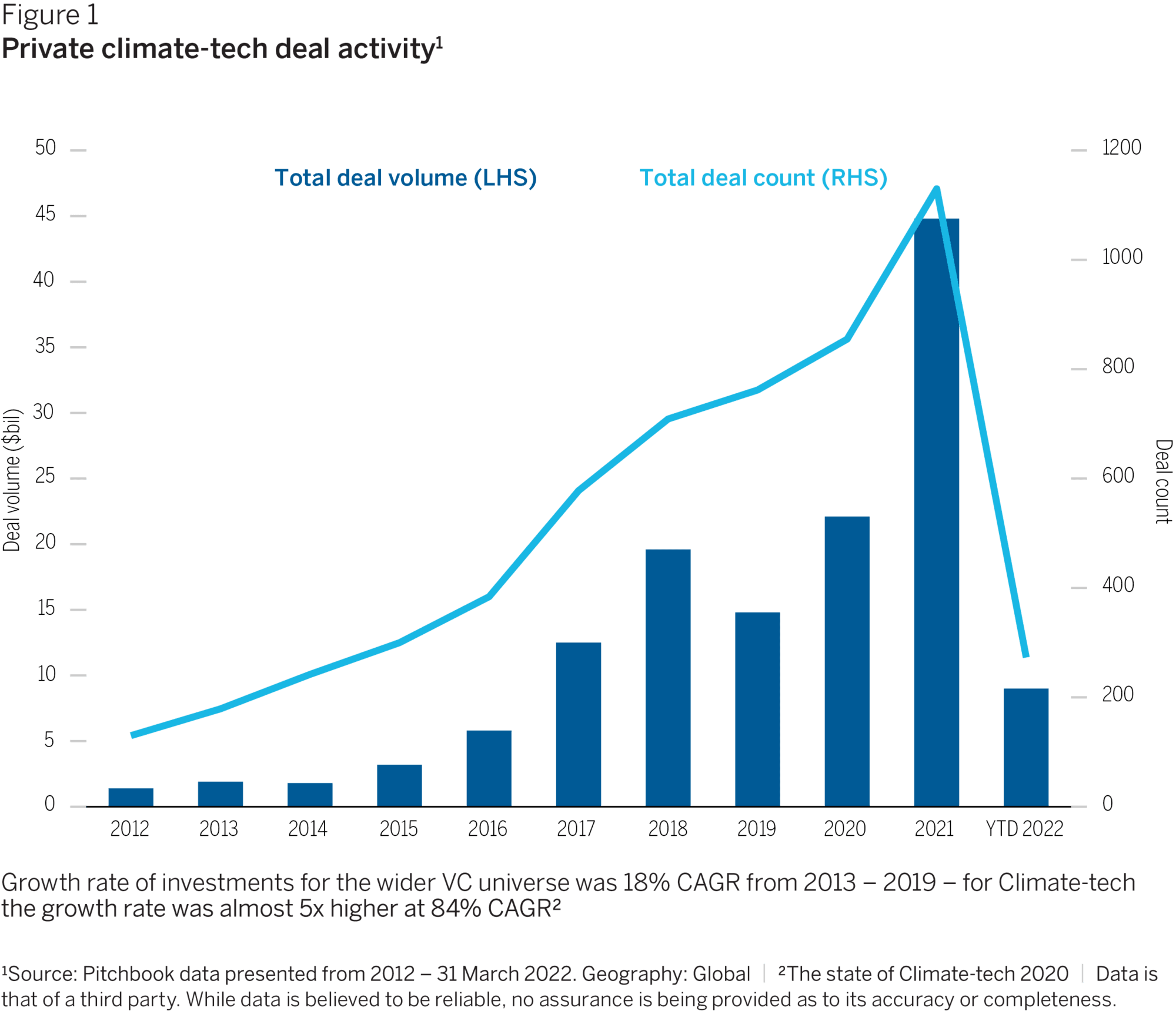

In our view, this creates an enormous opportunity for innovations and technology that address climate change while delivering a superior user experience without trade-offs. We believe venture-backed start-ups will be instrumental in developing many of these solutions, and they will likely require substantial growth capital to do so at scale. We see all of this reflected in the growth of private climate deal activity globally (Figure 1).

We sense growing optimism in the potential for innovation in the venture capital community as it joins with governments, scientists, consumers, and companies to find real solutions to climate change. We also think several secular trends are supportive of disruptive climate-focused entrepreneurs.

For example, as the list of countries and corporations committed to net-zero emissions continues to grow, we expect high levels of global infrastructure spend, creating a foundation for innovative, asset-light companies to build on.

In addition, consumers are demanding transparency and choices that match their climate-related values, and companies are in search of innovation that can help them meet that demand.

Cost declines and increased market adoption are continuing in well-known areas such as renewables and electric vehicles, are likely to continue with ongoing scientific innovation, for example, advances in solar materials and battery technology. These type of developments will be critical to the evolving market, but they also tend to be asset heavy and capital intensive.

Fortunately, there are also less capital-intensive solutions involving the application of existing technologies in end markets, which can drive efficiency while also reducing GHG emissions or increasing resilience to climate change. Sensors, connectivity, computing/analytics, artificial intelligence, and enterprise software and financing models, for example, can lead to smarter buildings and homes, connected and flexible energy grids, optimized manufacturing and supply chains, and new distribution and business models in the food and apparel sectors. Many of these business models help mitigate climate change not just by greening the supply of consumables but also by changing and optimizing demand.

Parametric weather insurance is emerging as a way for businesses and consumers to hedge their revenue or asset risk around weather-related risks.

Regarding adaptation, improved near-term weather and longer-term climate forecasting should help companies adjust their operations in real-time to account for extreme weather events and to incorporate future climate risk into long-term asset planning. Parametric weather insurance is emerging as a way for businesses and consumers to hedge their revenue or asset risk around weather-related risks.

Many of these tech-enabled solutions are likely to play an increasingly pivotal role in the battle against climate change. Less capital-intensive than infrastructure, we believe they represent a large and growing opportunity for private venture and growth equity.

We believe venture-backed start-ups will be instrumental in developing many of these solutions, and they will likely require substantial growth capital to do so at scale.

Broad investment flexibility

• No benchmark orientation; few investment restrictions

• Geographic, sector, market cap and asset class emphasis may shift over time

Liquidity risk

• Portfolio of illiquid/private companies

• The return of invested capital may be dependent on the success of the companies held in the portfolio and the timing of such liquidity is uncertain

Sector risk • May concentrate by sector; potential for lack of diversification

Country/currency risk • May concentrate by country

Transparency risk

• Holdings, pricing, and other data may be limited, and, thus less transparent than certain other investments

Please refer to this important disclosure for more information.

Market risk

• Directional; not market neutral

• Primarily invest in equity

• Will experience equity-like volatility, at times

• At times, markets experience great volatility and unpredictability