Carol Alexander, Professor, University of Sussex

Crypto is the most rapidly evolving asset class in the history of financial markets. Recent innovations in volatility products are at its most cutting edge. My talk for QuantMinds in Focus on May 27 begins with an overview of the state-of-the-art in crypto options as of May 2021 and an update on the bitcoin implied volatility index (BVIN), which I introduced at the last QuantMinds International in Hamburg, 2019. Thereafter I’ll be previewing two unpublished research papers about bitcoin options: one on the best models for market makers to use for dynamic delta hedging; and the other on net buying pressure and the type of information that is revealed by high-frequency traders in bitcoin options. This article reviews just the first part of my talk.

BVIN is a 30-day implied volatility index which is constructed using a similar methodology to CBOE’s VIX – except that extra data filtering is needed because of the irregular issuance schedule of bitcoin options on the Deribit exchange, and the uneven trading volumes on the maturities straddling 30-days. More information about its construction, including a detailed description of the methodology for live streaming the index every 15 seconds, is available from CryptoCompare.

Launched in 2020, BVIN was the first live-streamed bitcoin implied volatility index. Several weeks ago, Deribit launched their own implied volatility index with the intention to list futures on it. If successful, this would open the door for asset managers to list a myriad of other volatility products – like the ETNs and ETPs that were hitting the equity headlines for the wrong reasons in 2015 because early investors did not fully understand the negative roll-yield inherent in S&P constant-maturity indices. Credit-Suisse’s now delisted TVIX, which featured 2x leverage, was a prime example. But that’s another story – bitcoin volatility ETNs (as least on regulated exchanges) will take another few years, given the current stance of the SEC.

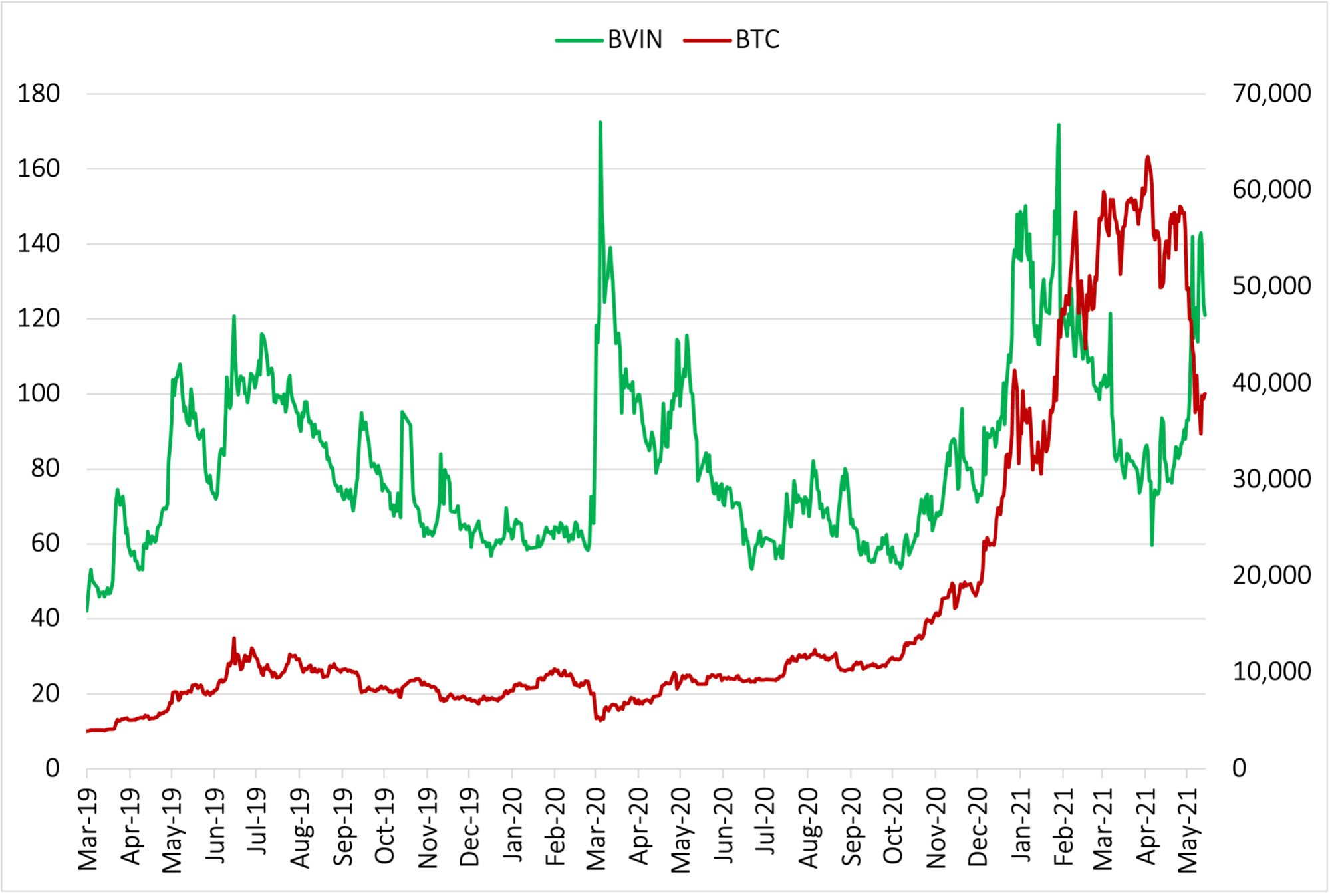

Figure 1: Bitcoin implied volatility index and bitcoin USD price

The VIX is child’s play compared with BVIN, which puts even the TVIX in the shade. For instance, after the COVID shock in March 2020 the VIX reached a maximum of only 67% (on 20 March 2020) and it has remained below 30% for at least the past year. Figure 1 depicts BVIN in percentage points (green, left-hand scale) and the price of bitcoin (BTC) in USD (red, right hand scale) from March 2019 until May 2021. BVIN has a baseline of around 60%, about three times higher than the VIX, and has an all-time high of 172% on 17 March 2020 precipitated by the Black Thursday across-the-board dive in crypto asset prices. It again exceeded 170% on 10 March 2021, but this time associated with a huge upward price jump from $30,000 to nearly $60,000, not a crash. At this point net buying pressure on OTM puts and ITM calls both went crazy on fears that the bitcoin price bubble would burst.

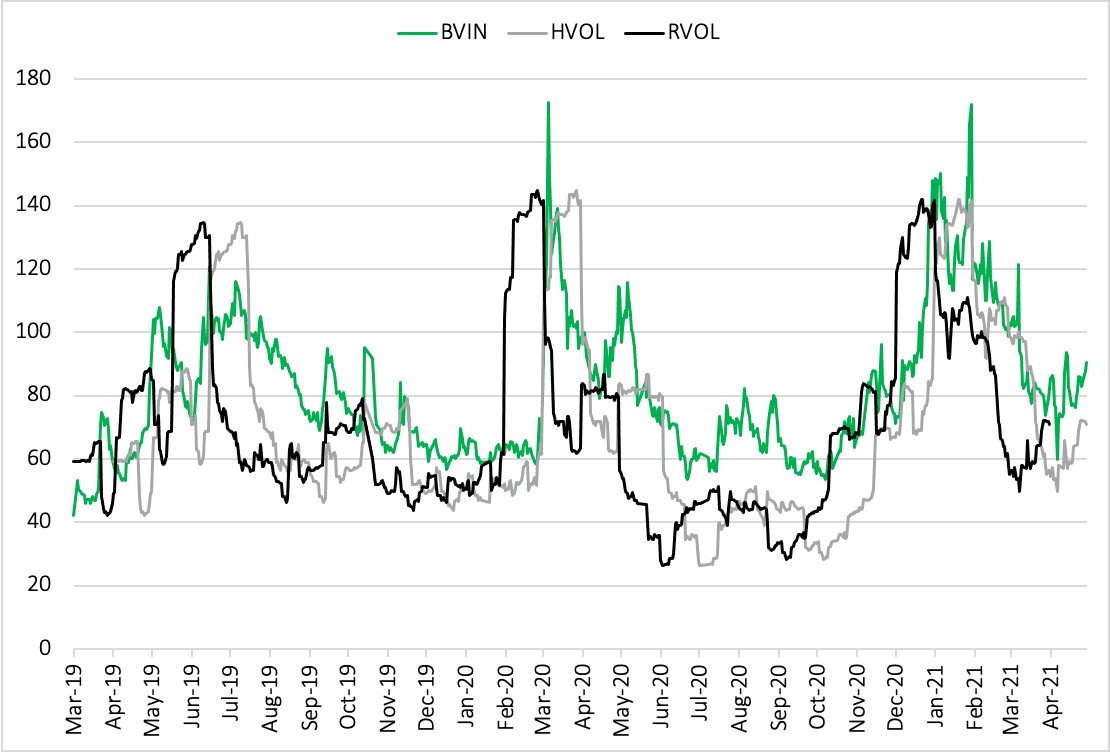

Figure 2: Bitcoin implied volatility index with 30-day historical and realised volatility

Figure 2 again shows the BVIN, plotted this time against 30-day historical (ex-post) and realised (ex-ante) volatility of daily log returns. It is the square of the realised volatility (RV) that is the floating leg of a standard bitcoin variance swap. Since July 2019, these products have been actively traded on-chain, which is the crypto equivalent of OTC. One can see from Figure 2 that a swap initiated in late February or early March 2020 would have been struck at around 60 – but the RV turned out to be close to 140!

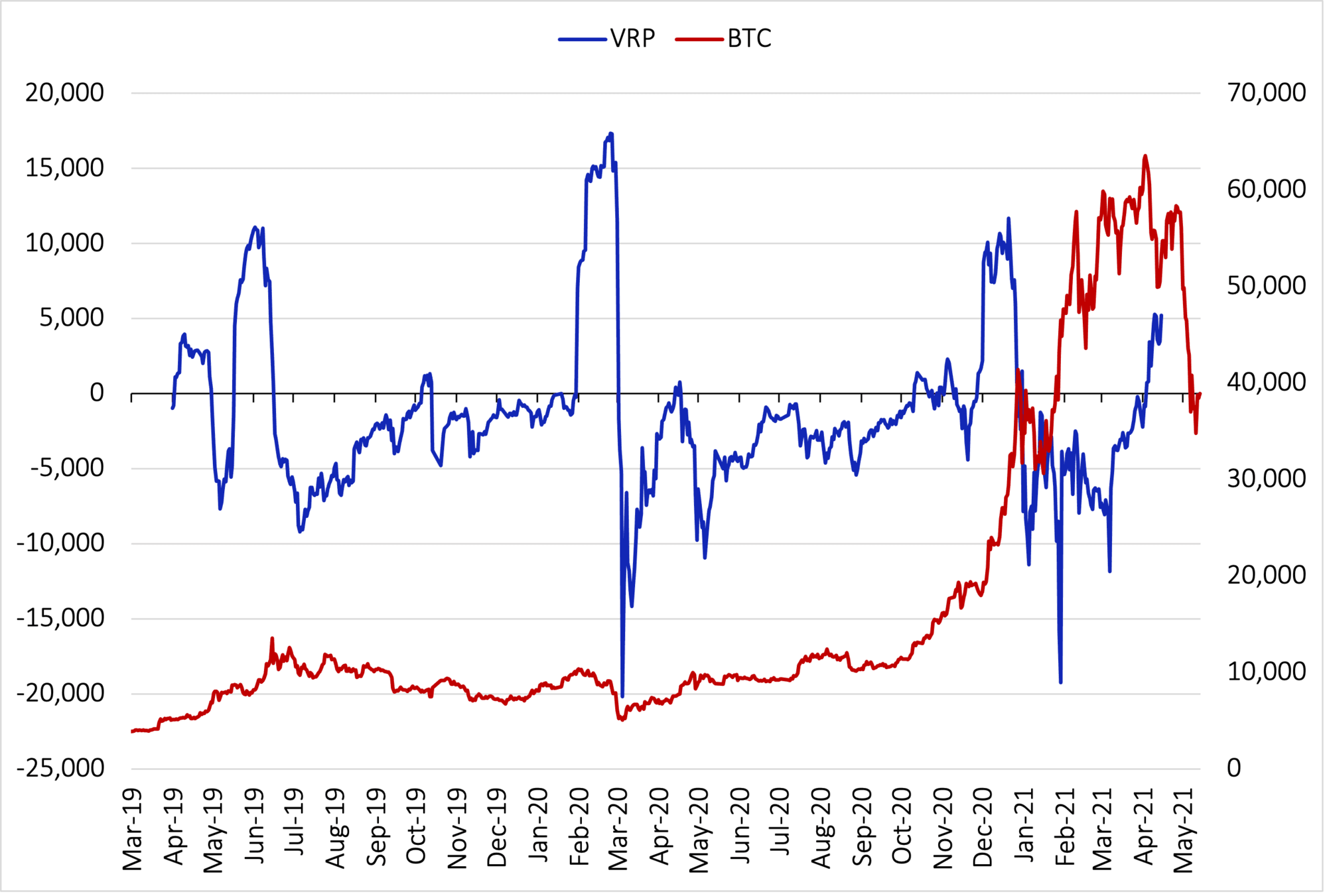

The BVIN is the fair-value of a 30-day bitcoin variance swap and, using this as the actual swap rate in the pay-off formula [RV2 – BVIN2] we obtain the blue line in Figure 3 below (VRP, blue, left-hand scale). This is the (fair-value) bitcoin variance risk premium which is the pay-off to just $1 notional on a 30-day bitcoin variance swap.

Figure 3: Bitcoin variance risk premium and the bitcoin USD price

Let us compare the bitcoin variance risk premium with that of the S&P500. A 30-day swap initiated on 1 March 2020 would have been struck at around 60 on bitcoin and at about 40 on the S&P500, not vastly different. But the bitcoin realised volatility turned out to 138% on bitcoin and (only!) 95% on the S&P. This way, the payoff to the floating leg of the bitcoin swap was over 15,000 per dollar notional, compared with less than 7,500 for the S&P500 swap.

At the time of writing, Deribit dominates trading in bitcoin options with a market share of over 80%. The CME also lists bitcoin options, but volumes there are tiny. Currently, bid-ask spreads on Deribit are far too high for effective volatility trading, ranging between 200 and 440 bps even for ATM options. However, these should come down as the competition from other exchanges increases. The original bitcoin options platform LedgerX is still fighting to retain just a small share of the market, but the largest crypto derivatives exchange Binance started listing American bitcoin options just over a year ago, and European options (with up to 10X leverage!) in December 2020. Binance is by far the largest of all crypto exchanges, with average daily trading volumes over all products reaching $50 billion so far this month. However, recent news of DOJ and IRS investigations of potential money laundering activities on Binance could damage this exchange, just as the CFTC’s investigation of KYC protocols did to BitMEX last year.

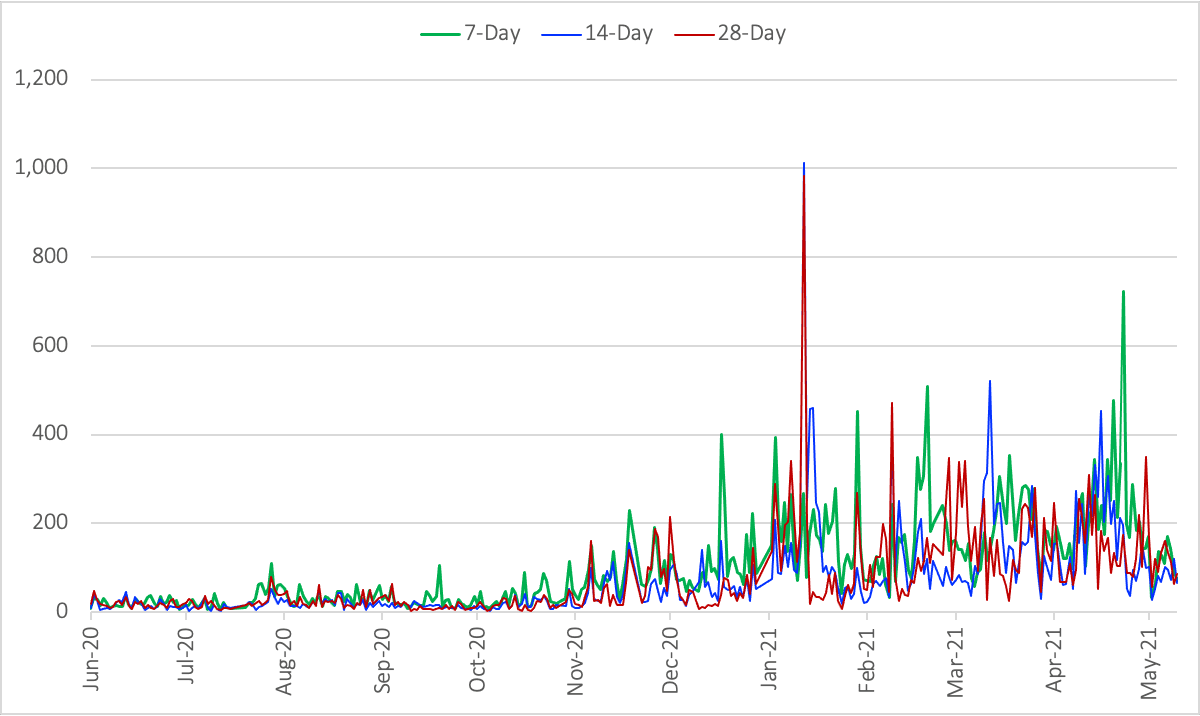

Even though unregulated crypto derivatives markets are open 24/7, volumes on bitcoin options are still not very large compared with the main CME markets for equities and commodities. For instance, Figure 4 depicts the evolution of the daily volume traded on Deribit bitcoin options at all strikes at a particular maturity, calculated as the sum of dollar notional x no. options per 24-hour period. We use linear interpolation to represent results as those for synthetic contracts having constant maturities of 7, 14 and 28 days.

Figure 4: Daily Volume Traded on Deribit Options (USD Million)

Compared with developed options markets, volumes are very small and shifted more towards the short end of the curve. Between January 2021 and the time of writing, the average daily trading volume was $185m at 7 days, $136m at 14 days and $142m at 28 days. Trading volumes are even lower at the maturities required for static 30-day variance swaps hedges, based on an index formula such as this. It is clear from Figure 4 that the bitcoin options market only really took off in November 2020, so my QuantMinds in Focus talk will be focussing on market makers hedging strategies and the information in the net buying pressures they are facing, since that time.

What does all this mean for pricing and hedging bitcoin volatility? Equity indices like the S&P500 have a variance risk premium that is usually small and negative. Hence, writing variance swaps on the S&P500 is rather like selling OTM puts – most of the time you make money on the premium and just occasionally you have to make a large pay-out. But the negative variance risk premium on bitcoin is much larger – most of the time, unhedged writers of bitcoin variance swaps would be raking it in – but the risks of huge pay-outs are larger and much more frequent than they are in equity indices, as we’ve seen in Figure 3.

So, the news is not great for bitcoin options traders or variance swap writers. Despite the considerable upside risk, the downside risks are catastrophic and remain difficult to hedge while volumes are still relatively low and trading costs are too high for optimal dynamic hedging. I’ll be watching developments in the DOJ and IRS investigations of Binance now. Deribit might become more or less competitive depending on the result.

Many thanks to Jimena Leon of CryptoCompare for preparing and providing the BVIN and BTC data for Figures 1 – 3 and to Arben Imeraj of the University of Sussex for preparing and providing the Deribit data for Figure 4.