Categories include shelf-stable groceries, frozen foods, nonfood and HBC, snacks and beverages

As grocery customers return to more in-store shopping, it’s clear that the online grocery shopping they embraced during the pandemic isn’t going anywhere any time soon.

Over 40% of shoppers currently order groceries online, according to Acosta research and 95% of them are ordering the same or more online than they did pre-COVID. “Looking ahead, online growth will slow as the vaccine allows shoppers to return to stores more comfortably,” acknowledged Jana Davis, senior director, business intelligence, Acosta. “However, with so many people now accustomed to the convenience of curbside pickup or home delivery, online grocery shopping will remain.” In fact, she added, eMarketer estimates that online grocery spend will reach $100 billion for the first time in 2021 and rise to as much as $200 billion over the next four to five years.

That bodes well for center store categories, which have surged online over the past year. Customers are far more comfortable buying items like paper goods, pet food, shelf-stable food and beverages and cleaning supplies online than they are trusting their fresh purchases to e-commerce.

“The widespread availability of e-commerce and the increased adoption rates post-COVID have influenced store guests’ behaviors and expectations,” said Joe McQuesten, senior VP, merchandising for retailer and distributor SpartanNash. “It is easier to trust the freshness and quality of center store items online, regardless of the retailer, and this commoditizes the center store portion of the basket more than the fresh. To differentiate themselves, retailers need to be creative with their digital center store experience by offering expanded ‘digital-only’ items and offers, unique pack sizes, an array of fulfillment channels and recurring order options.”

Continued on the next page

Supply chain challenges

Still, despite the continued elevated sales in center store — or perhaps because of that — not all the news is good.

“Right now, we expect center store categories to be largely impacted by supply chain shortfalls,” said McQuesten. “As the greater population returns to a post-COVID normal, we are just starting to see the economic effects of the pandemic, and one of those is a labor shortage affecting manufacturing and logistics. This is continuing to put pressure on an already fragile supply chain that hasn’t fully recovered from the COVID buying habits.”

Acosta’s Davis agreed. “We are witnessing huge pressure on the CPG supply chain this year that may not only impact shelf availability but will also drive up costs that will be passed on from the manufacturer to the retailer to the consumer,” she said. Still, on the positive side, these supply chain challenges create an opportunity for retailers to rethink center store.

“Both manufacturers and retailers will continue to focus on profitable sales growth, which requires increased focus on the role of innovation, efficient assortment, supply chain efficiency, private label strategy and demand creation,” Davis said.

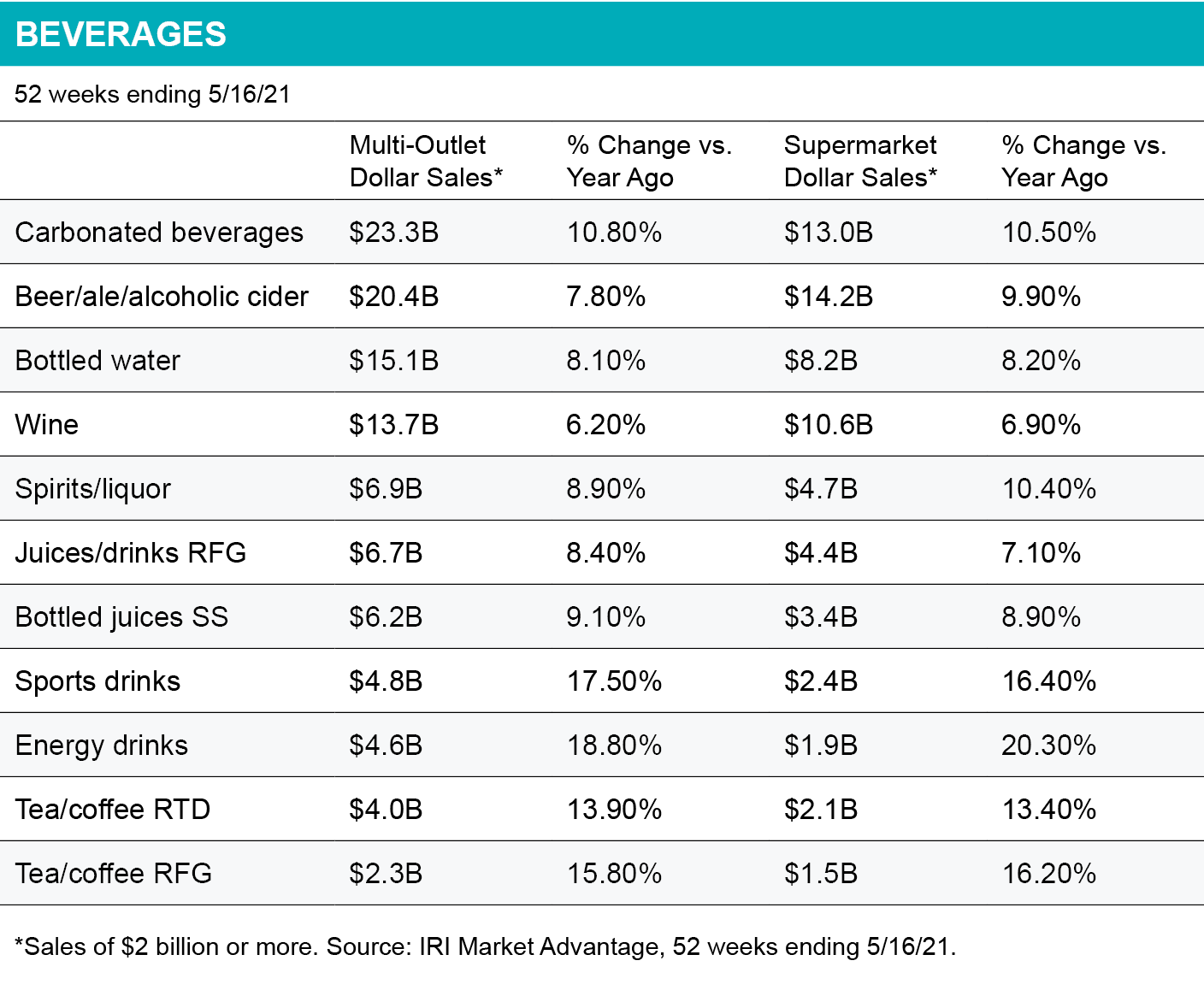

The flood of beverage sales that characterized 2020 has begun to ebb and flow in new patterns, as consumers appear to be stocking up on fewer cases of bottled drinks and turning their attention back to single-serve and grab-and-go options.

Overall, however, beverages sales remain strong, with double-digit sales gains in many categories for the 52 weeks through May 16, according to IRI data. Perhaps more importantly, beverages are also showing strong gains year-to-date compared with pre-pandemic sales levels, said Sally Lyons Wyatt, executive VP and practice leader, client insights, at IRI.

That’s particularly true for sports drinks and energy drinks, which in 2021 are seeing significant sales growth compared with 2019 levels, after not performing as well as some other beverages in 2020.

“People are out and about, they are exercising, and those items are having a banner year this year,” Lyons Wyatt said.

Jana Davis, senior director of business intelligence at Acosta, said she expected that sales of shelf-stable beverages to “continue at a strong pace” in the year ahead.

“Much of the growth has been driven by people working from home, and this trend will also continue, with one in five workers saying that they may work from home permanently,” she said.

She said bottled water sales are projected to grow nearly 4% in 2021, and said shelf-stable juice/drink sales will be on par with 2020.

Consumers are also looking to functional beverages for the health benefits they provide, said Joe McQuesten, senior VP of merchandising at SpartanNash.

“They are looking for functionality in the health and wellness sectors through enhanced waters, sports drinks and shelf-stable juices,” he said.

Charlotte Myer, divisional merchandise manager of grocery at FreshDirect, agreed, saying the online retailer sees better-for-you and low-sugar options in soft drinks and iced tea trending, as well as functional beverages offering immunity and other health benefits.

She also said consumers shopped for more multi-serve SKUs of some beverages, as opposed to multi-packs, as the pandemic wore on, particularly in categories that include cold brew and iced coffee, iced tea, and juice.

The trend continued in 2021, Myer said, but as restrictions on businesses and social distancing have loosened, consumers have been putting more single-serve beverages into their online shopping carts.

In the company’s office-delivery business, FreshDirect saw demand shift exclusively to single-serve options throughout the entire pandemic period, she said.

“As offices reopen, I expect to see increased demand for larger case formats,” Myer said.

Cheers to adult beverages

Within the alcoholic beverages and mixers category, grocery retailers saw strong sales during the pandemic amid the widespread closures of bars, but retail sales have remained elevated even as bars have reopened.

“Shoppers are looking to beverages as a key part of socializing with friends and family,” said McQuesten. “We are seeing this trend in the adult beverage category; as COVID-related restrictions lift and people get together again, sharing a drink to socialize and interact is regaining popularity.”

Davis of Acosta projected 2% sales growth in adult beverages in 2021, vs. 2020.

Lyons Wyatt said she expects consumers to continue practicing their cocktail-making skills at home to some degree, which bodes well for grocery retailers.

“I believe that you're going to see a falloff, obviously, versus a year ago because bars have opened back up, but I do think there's still going to be an elevated at-home occasion,” she said.

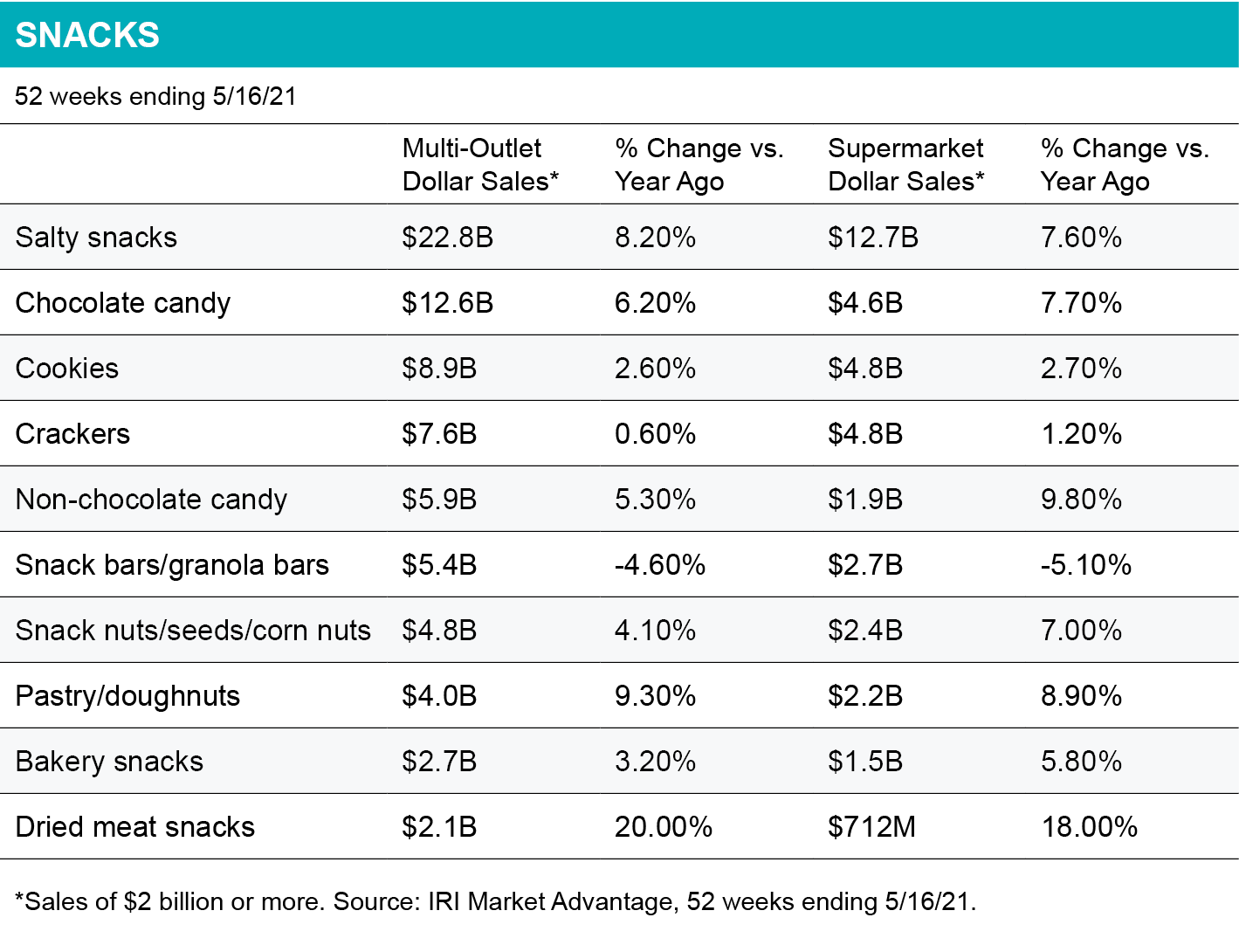

For younger consumers in particular, snacks are the new lunch. And breakfast. And dinner.

Gen Z’ers and Millennials are snacking more often throughout the day, often at the expense of eating traditional meals. This is helping drive snack-food sales and support an optimistic outlook for the category’s ongoing success.

“The snacking category was already rising before the pandemic, and we are predicting that increased snacking habits and occasions are here to stay,” said Jana Davis, senior director, business intelligence, Acosta. “Consumers will continue to seek indulgent snacks and comfort foods, but will also be looking for health-oriented options — think plant-based, immunity-boosting, high-protein — as well as convenient, on-the-go items, now that the stay-at-home days are behind us.”

She cited popcorn snacks as an example, projecting growth of 18% for the category in 2021, compared to 2019.

Cooking fatigue may also be helping propel the snack category, said Charlotte Myer, divisional merchandise manager for grocery at FreshDirect, who said consumers seem to be opting for the convenience of having snacks around the house to replace traditional meals.

“Sweet and salty snacks both saw elevated volume during the initial pandemic pantry stock up period, but unlike categories like canned goods that flattened out into the summer months, sweet and salty snack demand continued to rise,” she said.

Comfort foods and indulgent categories such as chips, cookies and chocolate showed the strongest growth in demand, Myer said.

In-store vs. online

As more and more consumers have emerged from sheltering in place and begun resuming pre-pandemic activities, the nature of snacking has been more on-the go, said Sally Lyons Wyatt, executive VP and practice leader, client insights, at IRI. That has impacted categories such as nutrition bars, which consumers often select as grab-and-go options, and which are now rebounding after a down year in 2020, she said.

Consumer shopping patterns are also impacting snack sales. As shoppers cut back on their store visits during the pandemic and loaded up on multipacks, they also were making fewer passes through the impulse display-filled checkout lanes, Lyons Wyatt said. That had a big impact on supermarket sales of items such as gum and mints last year, although they have bounced back in 2021, she said.

Consumers have increasingly opted for self-checkout, curbside pickup or delivery, where capturing impulse snack sales can pose significant challenges for retailers.

In a webinar on snacking earlier this year, Lyons Wyatt said 9% of snack sales occurred online in 2020, up four percentage points over 2019 levels.

E-commerce sales of snack nuts, seeds and corn nuts, which were already more prevalent online than other snack foods, rose seven points in 2020, to account for 15% of total sales for that segment. Online sales of salty snacks, meanwhile, rose three percentage points last year, to account for 6% of total omnichannel sales of salty snacks.

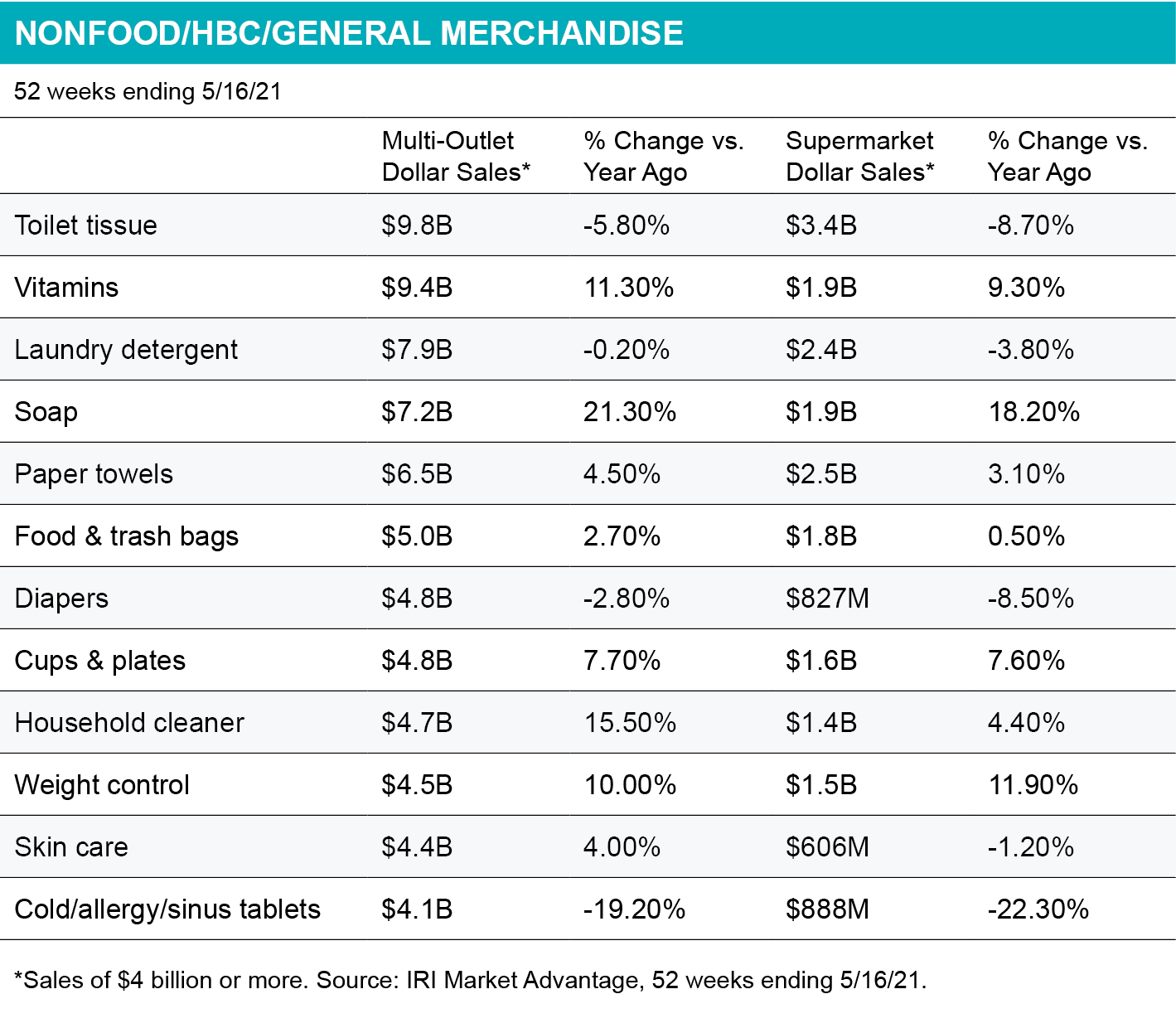

Wearing masks and social distancing have proven to be highly effective at limiting the spread of COVID-19, the flu and the common cold, and also at limiting the sales of the medications used to treat these illnesses.

Retailers saw sales of cold/allergy/sinus medications, both liquids and tablets, plunge in double digits in the 52 weeks through May 16, although items sold for preventative care — immunity boosters and vitamins, for example, have performed well. Consumers have more recently looked to products that help them control their weight after a year of staying home noshing on comfort foods and home-baked goods.

In other nonfood categories, most paper goods, detergents, soap and household cleaners retained their elevated sales, although toilet tissue saw a drop of nearly 10% since a year ago — a natural decline given the skyrocketing sales early in the pandemic.

Health push

The pandemic didn’t really slow consumers’ increasing focus on health and wellness.

“During the COVID-19 pandemic, health and wellness became a top priority for many people,” said Jana Davis, senior director, Business Intelligence, Acosta. “We expect this focus to continue, which should propel sales for nutrition and weight-control products through 2021.”

The concept of “self-care” also escalated during the pandemic, she said, noting that about two-thirds of shoppers said they use vitamins and supplements to manage their physical health.

She said that Acosta has recently observed a slight shift away from nutritional snacks and diet/weight control products to sports nutrition.

“Growth has mainly been driven by powders, but shakes and bars are also on the rise — both in store and online,” she said.

The vitamin category, like many other categories throughout the store, has been hit by supply shortages, said Charlotte Myer, divisional merchandise manager, grocery, at FreshDirect.

Key vitamins such as vitamin C, and immunity-support products such as Emergen-C and multi-vitamins, were depleted after consumers stocked up during the initial phase of the pandemic last year, she explained.

More recently, consumers have been seeking immunity-boosting products and products with natural or botanical ingredients to maintain their health, Myer said. She said the online retailer has seen consistent demand for some dietary supplements, citing sales increases of 62% in the last 52 weeks.

Consumers are also seeking products that support cognitive health and sleep aids, as well as minerals such as magnesium and zinc, she said.

Vitamin boost

Vitamins have been the No. 1 growth category in the HBC department at SpartanNash, said Joe McQuesten, senior VP of merchandising. Other growing categories include pain relief, stomach remedies and first-aid items.

Among vitamins and supplements, melatonin and vitamin D have been showing strong growth, he said. Apple cider vinegar gummies, touted for gut health and other benefits, have also seen significant sales growth. Overall, gummies and soft gels have represented almost 70% of the growth in this category in the latest 26 weeks, he said.

In the weight control products category, McQuesten said consumers appear to be focused on weight management, as opposed to weight loss. He said ready-to-drink diet and protein-based products have been showing growth, and that customers have been gravitating toward multi-packs of nutritional bars and products that make keto-friendly claims.

Many consumers seemed to discover in 2020 that the frozen department of the supermarket is not a vast Arctic wasteland, but instead a rich trove of flavorful, convenient treasures.

“During the pandemic, consumers revisited the frozen food categories for easy-to-prepare meal solutions, and many were excited to discover that the frozen foods aisle offered increased innovation and great-tasting, easy-to-prepare meals for all households,” said Joe McQuesten, senior VP of merchandising at SpartanNash.

He said he expects elevated sales to continue in the frozen categories, although at a slower pace as consumers return to their pre-pandemic dining patterns, with increasing restaurant visits.

“Innovation and promotional activity are key to continued success within the frozen food categories, with healthier protein-based meals along with multiple price points creating a stock-up event,” he said.

Jana Davis, senior director of business intelligence at Acosta, said the convenience and value of frozen foods, along with innovations in taste and quality, will help support the category going forward.

“Frozen products — particularly produce, pizza, snacks and entrees — will likely remain top of mind for shoppers in the coming months,” she said, citing predictions that many families plan to continue eating together at home at least as often as they do now.

The popularity of frozen foods among younger consumers in particular bodes well for the category, said Sally Lyons Wyatt, executive VP and practice leader, client insights, at IRI.

Online sales of frozen foods have continued to perform well in 2021, she said, although sales in brick-and-mortar have declined, compared with the spring of 2020, when consumers were stocking up on core proteins.

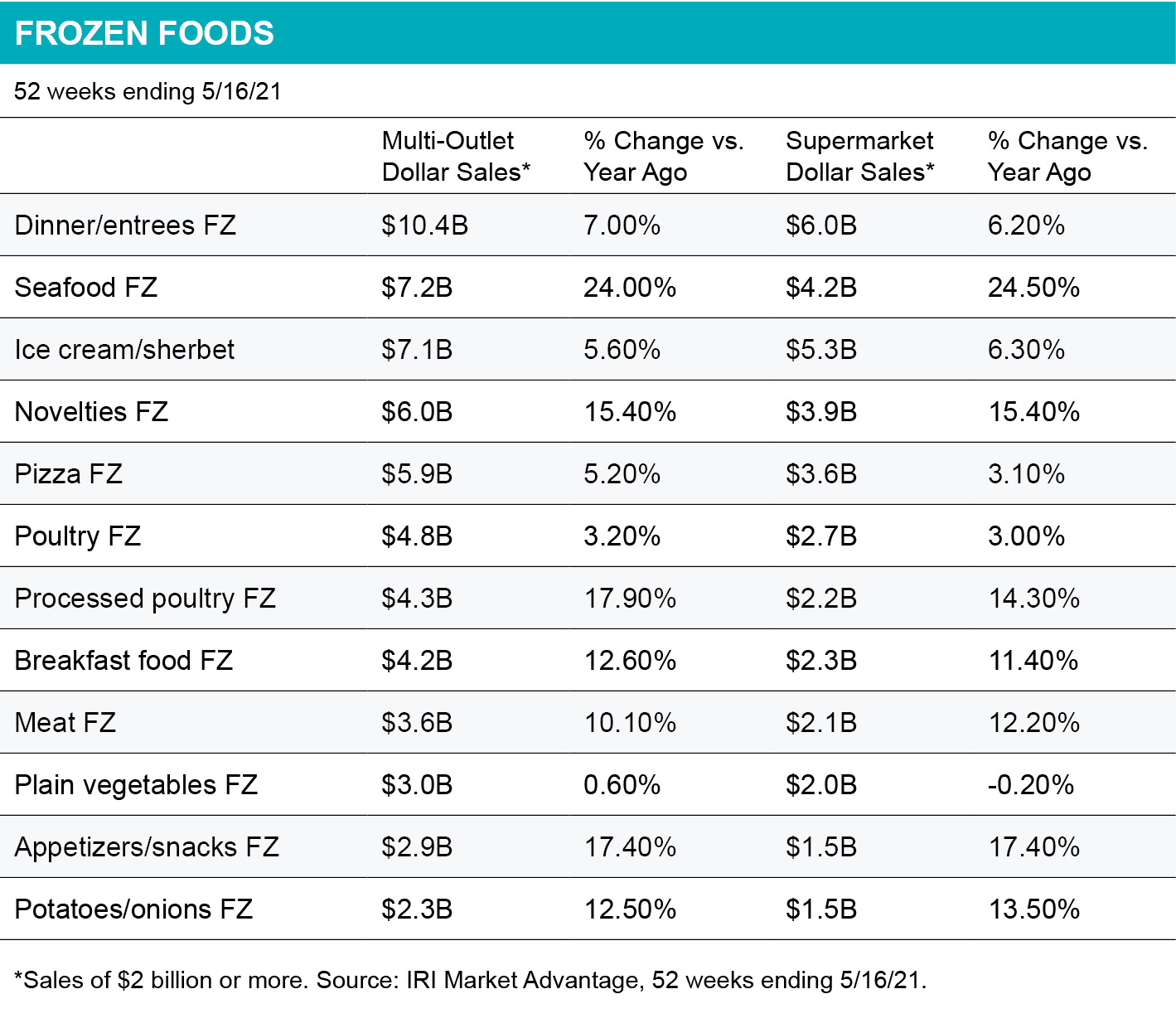

The frozen category is still showing “incredible growth” compared with 2019, however, Lyons Wyatt said, citing frozen novelties and pizza in particular. Sales of frozen novelties were up 15.4% in supermarkets for the 52 weeks through May 16, compared to the year-ago period, according to IRI.

“People wanted to treat themselves, as well as just indulge in nostalgia, or indulge in their favorite treats,” she said.

Frozen seafood was also a big winner during the pandemic and has continued to perform well, with sales up 24.5% in supermarkets for the 52 weeks through May 16.

Building meals with frozen

Sales trends in frozen foods among different classes of trade appeared to illustrate how consumers have been shopping this category, Lyons Wyatt said. Consumers tended to use supermarkets’ frozen departments to fill a wide variety of their needs, including both meal solutions and treats, while they turned to club stores and mass merchants for larger pack sizes of both meal ingredients and certain other frozen items, such as berries — presumably to be used for making smoothies at home.

Evidence that consumers have appreciated the convenience of frozen foods as meal-builders also appeared in the 2021 Power of Frozen Food Report from the American Frozen Food Institute. Its research showed that among the 57% of frozen-food consumers who bought more frozen foods during the second wave of the pandemic last fall than they did before the pandemic, 82% said they were driven by meal planning for dinner, 55% said they were buying frozen to fulfill lunch plans, and 42% said they were buying frozen for breakfast meals.

Other occasions that were driving frozen purchases were snacks (43%), desserts (28%) and beverages/smoothies (13%).

Consumers not only learned how to navigate Zoom during the pandemic, but it appears many also learned their way around the kitchen for the first time.

Sales patterns in the shelf-stable grocery category indicate that home cooking — including some degree of the home baking that soared in 2020 — is continuing at an elevated level in 2021.

Charlotte Myer, divisional merchandise manager, grocery, at online retailer FreshDirect, said consumers who are adopting new behaviors continue to drive sales of some dry grocery items, especially those that offer convenience and assist in meal preparation.

“People certainly aren’t baking at the same rate that they were in May of 2020, but they are definitely baking more than they did in 2019, indicating that many of these changes in consumer behavior are here to stay,” she said.

During the pandemic, consumers not only purchased more baking ingredients, but also meal-prep solutions such as boxed mac and cheese, heat-and-eat meals and shelf-stable simmer sauces, she said.

“All of these were driven by the consumer shifts, first to cooking as a source of comfort, and then, as cooking fatigue set in, a need for easy ways to get a nutritious meal on the table,” said Myer.

“Similar to the trends we see elsewhere in the store, better-for-you or mission-driven brands continue to take share from their conventional counterparts, as conscious consumerism plays a bigger role,” she said. “This trend has been in place for years but accelerated in 2020 and continues into 2021.”

Joe McQuesten, senior VP of merchandising at SpartanNash, predicts that consumers will increasingly shift from home baking toward premade baked goods.

“We expect the high demand of key stock-up categories, including baking, to moderate in a post-COVID world as store guests seek convenience-oriented baking products,” he said. “As we look at the long-term changes in shopper behavior, we know that baking indexes as a long-term habit change — especially during the holidays —so we expect to see elevated demand.”

Sally Lyons Wyatt, executive VP and practice leader, client insights at IRI, said many shelf-stable products are continuing to grow their online sales, even as brick-and-mortar sales taper off compared with year-ago levels. Sales of many of these pantry items are still up in 2021 compared with two years ago, however.

“Baking, for example, is definitely down versus a year ago, but up versus two years ago, which means there's still a little elevated baking in the home,” she said. “You've got these inner chefs that were realized last year.”

Coffee at home

Coffee is following a similar pattern, she said. While at-home coffee consumption increased significantly during the stay-at-home periods last year, many consumers — but not all — have since started venturing out of their homes again for their daily dose of caffeine, while others are continuing to buy grounds and whole beans at the supermarket.

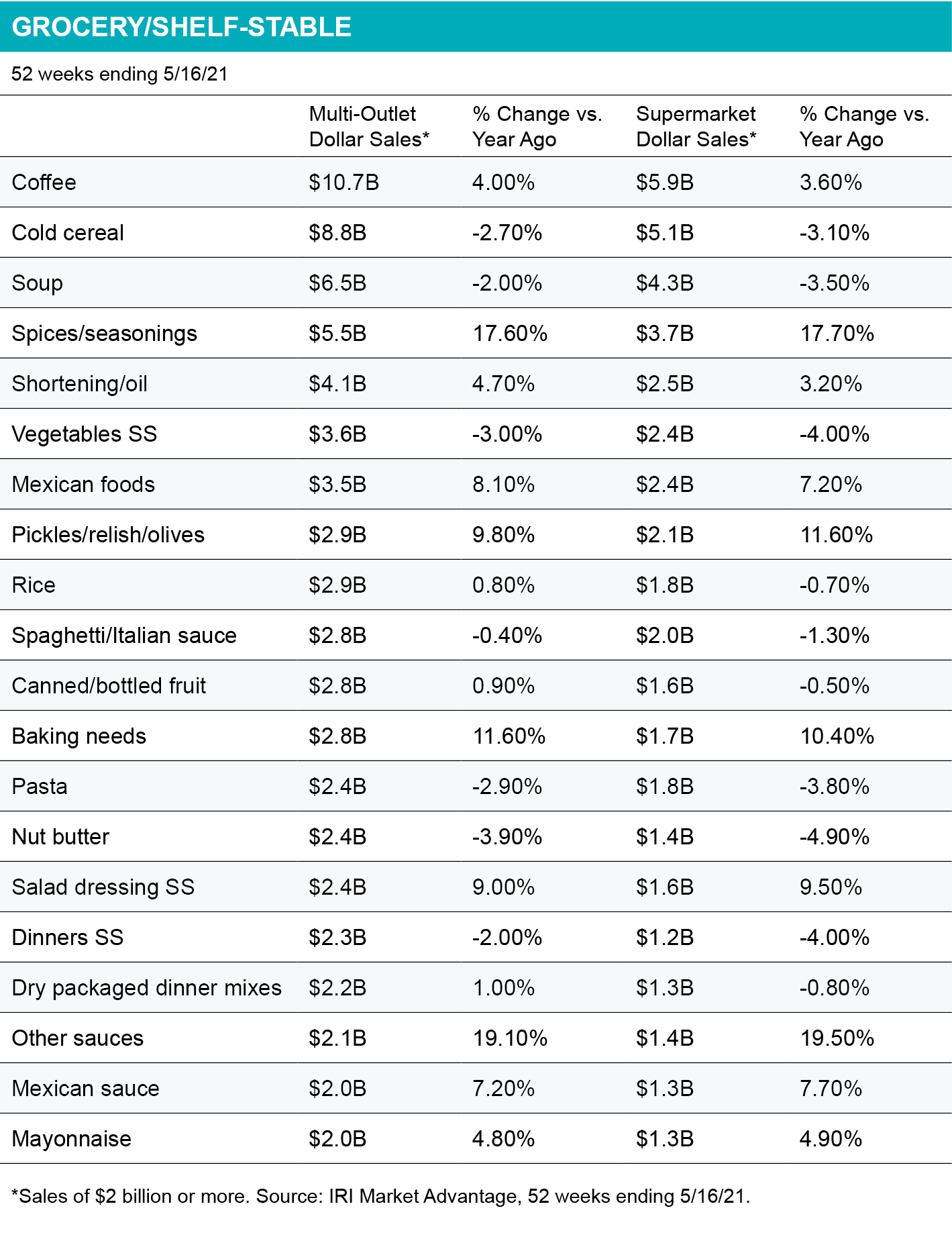

While coffee sales were up 3.6% for the 52 weeks through May 16, they have been down about 3% year-to-date, Lyons Wyatt said. But coffee remains the No. 1 grocery item at supermarkets by sales, by a comfortable margin over cold cereals, the next biggest category. Retail sales for coffee are still up versus 2019 levels, Lyons Wyatt noted.

“That’s the key,” she said. “There are still elevated at-home coffee occasions versus 2019, just not as many versus a year ago.”